When it comes to lithium stocks, I really only have two ideas that I like in the space right now. The first, I have discussed on this blog extensively, both here and here. But when it comes to my second favorite lithium stock pick, I have only shared extensive details with subscribers so far.

Well, as anyone who has been paying attention to mining stocks knows, the sector is currently in disarray right now, all across the board (gold, silver, lithium, etc.), so now is as good a time as any, I guess, to dive into the details…

But before we get started, let’s provide a quick backdrop to gives readers some context as to why I’m so bullish on lithium stocks in the first place…

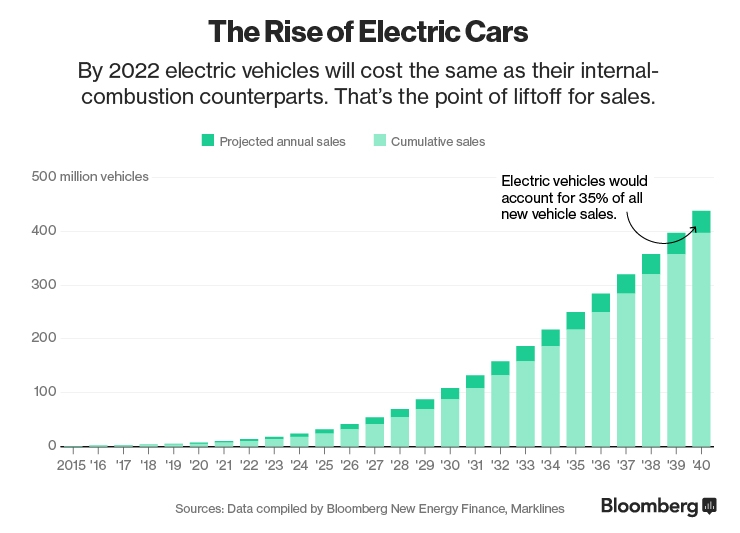

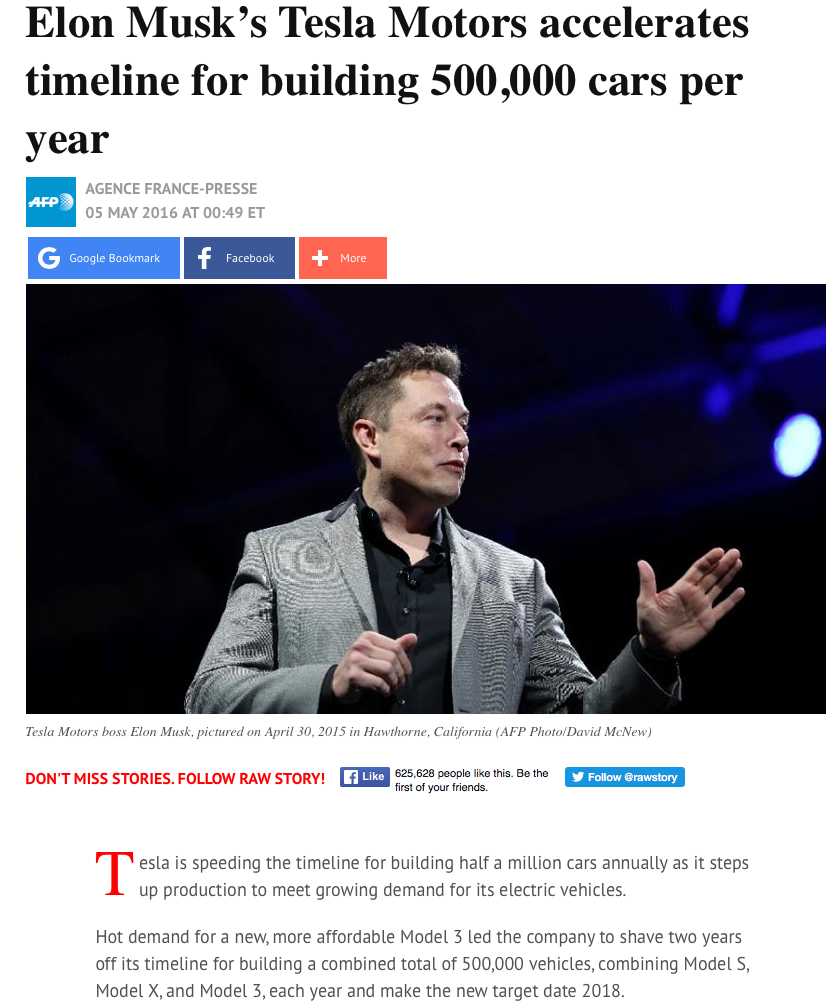

Unless you’ve been living in a cave the last year, most everyone is now aware of the clean energy/electric vehicle (EV) revolution that is taking place in the world, being spearheaded by Tesla and their Model 3 sedan.

You can find my full thoughts on lithium/clean energy both here, and here, but to quickly summarize:

From RawStory:

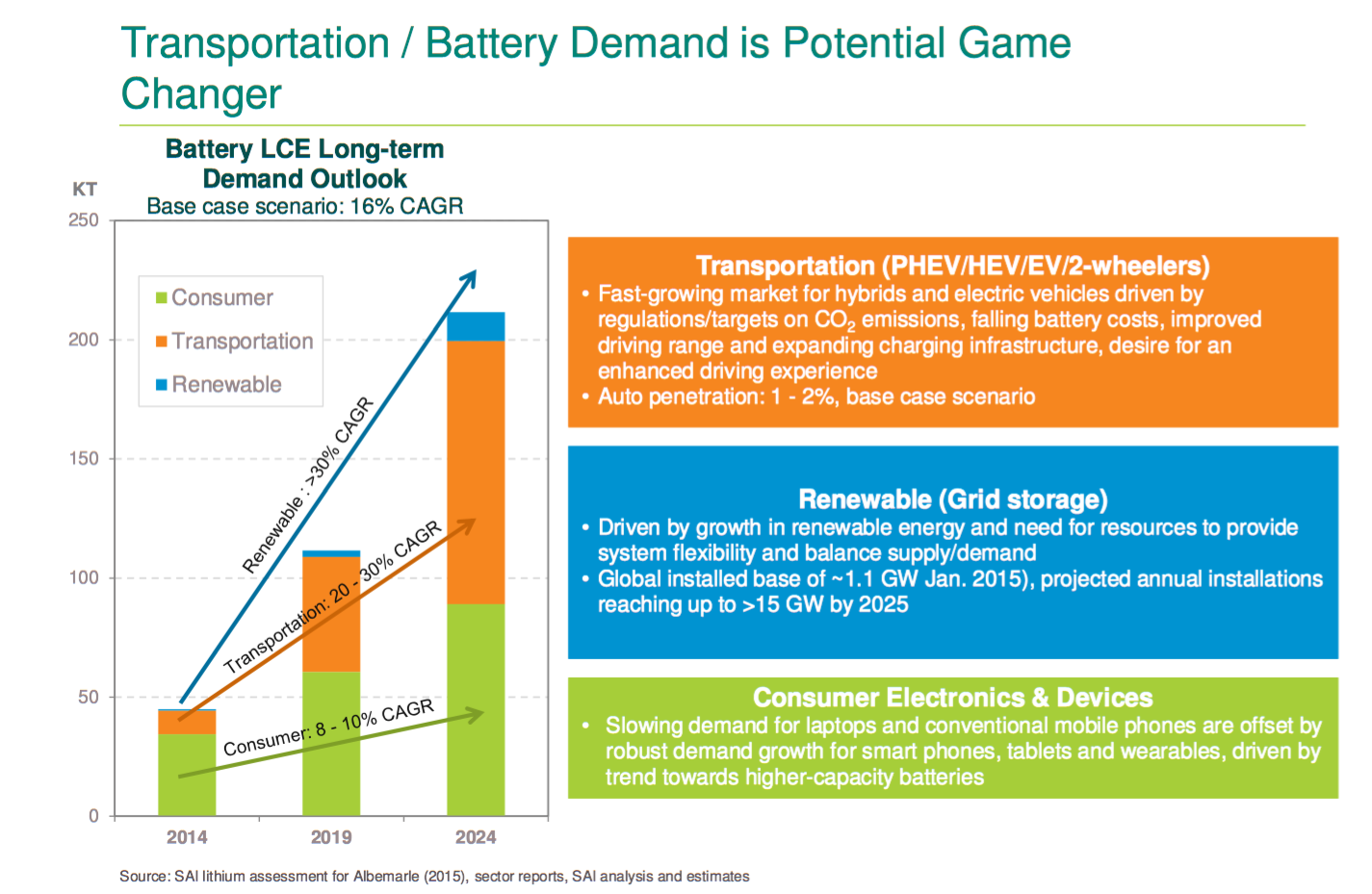

From Albemarle:

In short, we are quickly entering into the Age of the Electric Vehicle.

- Disruptive Technology.

- A new revolution.

- Hyper-growth.

Demand for EVs is rapidly increasing — As shown in the slide above, Compound Annual Growth Rate (CAGR) for electric vehicles will be in the double digits for the foreseeable future…

Tesla and its world-class salesman Elon Musk will hype the story and get the masses interested (they are quite good at doing that)…

https://www.youtube.com/watch?v=7HOhOeKwe30

Whereas China (as usual) will do the actual heavy lifting and be the catalyst that drives the bulk of demand/sales for EVs.

Elon Musk and China — That’s a pretty potent tag-team that works for me!

Anyway, as far as I’m concerned, there are really only two ways to make a lot of money with investing — Deep Value Investing (e.g. precious metals stocks in 2015) and Hyper-Growth Investing (e.g. AAPL, GOOG, AMZN).

As it pertains to lithium stocks, I am very much focused on Hyper-Growth.

However, like I mentioned in the beginning of this article, right now, I have two ideas that I think can provide investors a combination of both Deep Value and Hyper-Growth.

Sound too far-fetched to believe?

Read on…

Critical Elements

Critical Elements (CRE.V/CRECF) is a junior development-stage company that is currently progressing its Rose Lithium-Tantalum Project in Quebec.

Learn more by watching this most recent presentation given by Vice-President Jean-François Meilleur at the Master Investor 2016 show in the UK.

Right off the bat, we are already talking about operating in a first world jurisdiction with ZERO geopolitical risks in Quebec… So, for any prospective investors looking for a “safe” lithium play, we are already getting off to a good start… before diving into the details.

Moving along, even though the company will be mining both lithium and tantalum, when it comes down to it, the “cash cow” in terms of revenue and free cash flow will come from its lithium products (due to elevated prices driven by the explosive growth in demand); you can think of the tantalum as being more of a “freebie”, or byproduct, which helps to raise the project’s Li2O Equivalent grade/tonnage, and to help offset cash costs… Further, tantalum is one of those elements that is tough to locate in “non-conflict” regions, so having this secondary product is definitely not a bad thing.

Rose-Tantalum Project

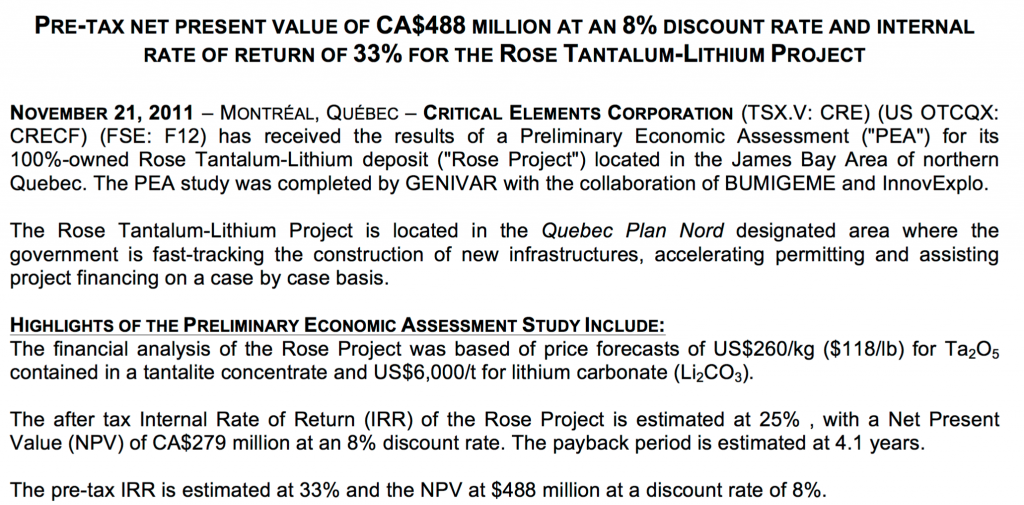

Although Critical Elements is not yet in production (and most likely a name you’ve never even heard of before), their Rose Lithium-Tantalum Project is by no means a new discovery; actually, the project already has a resource (Preliminary Economic Assessment), which was published long ago, back in 2011.

From Critical Elements.

From Critical Elements.

Critical Elements Corp. began drilling the Rose property in late 2009. A total of 181 drill holes totalling 26,500 metres have been drill to date on Rose Deposit.

The Rose deposit has been well drilled out and delineated over the years… Moose pasture, this land is not.

From Critical Elements.

The PEA shows project economics demonstrating a decent pre-tax Net Present Value (NPV) of C$488 million (post-tax of C$279 million), and a pre-tax Internal Rate of Return (IRR) of 33% (post-tax of 25%), using an 8% discount rate, but keep in mind, this takes into account a lithium carbonate sales price of only $6,000/t.

Rising Lithium Prices

Most recently, in 2016, we’ve witnessed a surge in the spot price of lithium products.

From The Economist:

From Pilbara Minerals.

Any price forecasts made by analysts should always be taken with a grain of salt, but nevertheless, it does appear plausible to assume that the price of lithium carbonate will reside north of $8,000/t for the near/intermediate term.

Revised Project Economics

The following slide shows revised economics for the Rose Lithium-Tantalum Project, but as noted earlier, these numbers are based on a 2011 PEA, not any Feasibility Study (FS).

So, use them as a rough estimate, at best…

From Critical Elements.

At a lithium carbonate sales price of $8,500/t (and tantalum at $118/lb), we could now be looking at a pre-tax NPV of C$1.085 billion, and pre-tax IRR of 53.3%.

Quite the upgrade, right?

Now imagine the scenario that could unfold if we do indeed witness a supply shortage in lithium (which some of the more bullish analysts are forecasting) and the price of lithium carbonate stays elevated above $15,000/t; the pre-tax NPV might possibly jump to C$2.6 billion and the pre-tax IRR an astounding 92%!

It gets better…

Risk vs. Reward

As I mentioned earlier, I feel that shares of CRE.V/CRECF can provide investors with a blend of both Hyper-Growth potential and Deep Value; the robust lithium carbonate prices explain the Hyper-Growth part of it, and the following slide will explain where the Deep Value lies.

The current market capitalization is less than C$50 million…

That’s peanuts!!

Right now, even in the exact same lithium space where Critical Elements operates in, you’ve got plenty of super early-stage junior exploration companies who don’t even have a defined resource (much less a drill hole punched into the ground) getting attributed that type of market cap valuation (or more)…

As readers know, whether we are talking about mining stocks, or any other asset class, I’ve learned to focus on the risk vs. reward proposition of any investing idea .

Right now, on the open market, any investor/speculator is able to purchase shares of Critical Elements, a company that could conceivably have a project that is valued at a pre-tax NPV of over C$1 billion (possibly even over C$2.6 billion) for less than C$50 million.

To me, that’s like presenting the following type of deal:

- Risk 50% of your principal to have a realistic shot of potentially making 500%+ gains.

These type of opportunities aren’t always so easy to find, and they’re the stuff that speculators dream of!

Of course, when it comes to development-stage projects, there are no guarantees! But think about it logically — If the risks were ZERO, would shares be selling at such a massive discount?

There are no free lunches when it comes to investing! If you want massive upside potential, you have to court risks… Period!

Now, let us assess the risks…

Strategic Partner

When it comes to risks, first off, it should be noted that Critical Elements has plans to become a vertically integrated operations; in other words, the company will not simply be mining spodumene (hard rock lithium) and selling spodumene concentrate to the markets. Instead, the company is proceeding to build a chemical plant to produce/sell both low iron spodumene concentrate (for the glass/ceramic markets) along with battery grade lithium carbonate (for the EV markets). And let’s not forget the byproduct, tantalum, which helps add further diversity to the revenue stream.

This has both pros/cons…

If you can manage to get to finish line in one piece, it may just be worth all the hassle… As shown in the slides above, chemical-grade spodumene concentrate (6%) is projected to sell for around ~$500+/t, but battery grade lithium carbonate commands a much more impressive $8,000+/t. When you vertically integrate, you get to cut out the middleman and reap all the benefits yourself… which is what Critical Elements is attempting to achieve here.

However, on the flipside, anytime you make things a whole lot more complicated, you also inherently introduce additional execution risks to the project… For starters, the CAPEX increases relative to non-vertically integrated projects (~$270 million from PEA), you need to become not only a mining expert but also extremely well versed in chemicals/processing, and you drastically delay your time to money because it takes many more years to get everything “just right” so that you can start producing product(s)…

Luckily for investors, Critical Elements was smart enough to know their own limitations and to have the sense to reach out to a proven expert in the field for guidance.

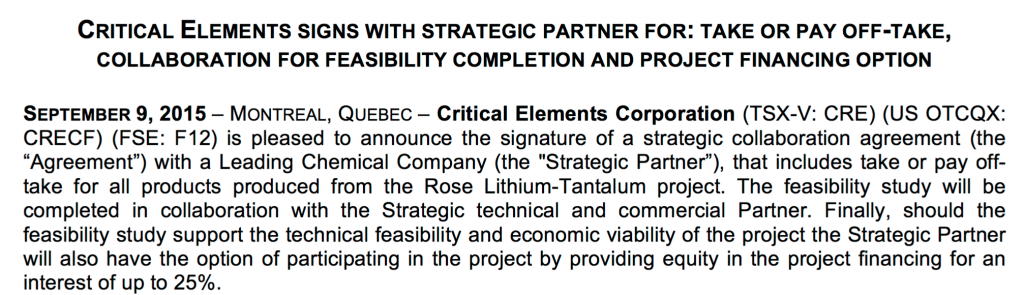

In September 2015, Critical Elements signed a take-or-pay offtake agreement with a “mystery” major chemical company.

Take or pay off-take Agreement

Subject to the take or pay off-take agreement to be executed by the parties (the “Take or pay off-take Agreement”), the Strategic Partner will have the sole and exclusive right to purchase all of the produced products including spodumene concentrate (technical and chemical grade), all lithium chemicals (carbonate, hydroxide, chloride), mica and tantalum concentrate (collectively, the “Products”).

The parties will use their commercially reasonable efforts to finalize and execute the Take or pay off-take Agreement by no later than 60 days following the completion of the feasibility study. Under the Agreement, and subject to certain conditions, notably the exercise of the Financing Option (as defined below), the Strategic Partner has also been granted a right of first refusal to become the exclusive off- taker for all Products on any of the future projects of Critical Elements (or its affiliates).

Feasibility Study

The Strategic Partner has agreed to collaborate with, assist and provide technical support to Critical Elements for the preparation and completion of the feasibility study. The Strategic Partner has further agreed to provide logistical and sales support to Critical Elements in relation to the distribution and sale of all future mineral products to be produced on the Project (the “Mine”).

Project Financing

As consideration for the Strategic Partner’s covenants and undertakings under the Agreement, Critical Elements has agreed to grant the Strategic Partner an option to acquire an ownership interest of up to 25% in the project by committing to pay for a portion of the mine construction costs (the “Financing Option”). The Strategic Partner may exercise the Financing Option within a period of 60 days after having received written notice from Critical Elements to the effect that it has arranged financing for mine construction. The Financing Option is subject to certain conditions, including the execution of the Take or pay off-take Agreement.

“This is truly a game changing Agreement for the Company,” said Jean-Sébastien Lavallée, President and CEO of Critical Elements. “The Company now has the ideal partner to complete its feasibility study and advance the Rose project.”

This was a major step in the right direction and a huge move made towards further de-risking the Rose Lithium-Tantalum Project for Critical Elements! Unlike commodities such as gold, silver, copper, etc. that are traded on major exchanges and have futures contracts/swaps, lithium trades via contracts (i.e. offtake agreements reached with end users/customers), so without one (some) secured, a producer is essentially dead in the water… and altogether useless.

As Critical Elements CEO Jean-Sébastien Lavallée stated above and in the following video below, this agreement was a monumental “game changer” for the company.

Again, great news! But despite the positive press release, I’m sure many investors were still skeptical of the Critical Elements story, especially given the fact that this strategic partner chose to remain anonymous at the time of the announcement…

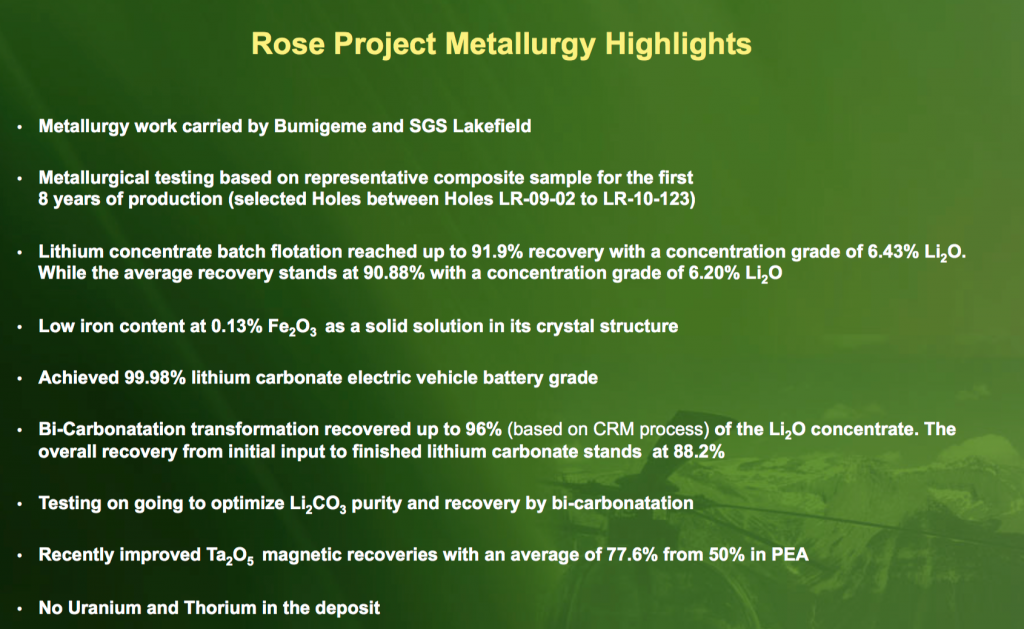

Metallurgy Highlights

Nevertheless, much progress has already been accomplished on the metallurgical/chemical front over the years, and no doubt, further refinements/advancements will be made in the future due to the addition of a proven expert partner into the fold.

From Critical Elements.

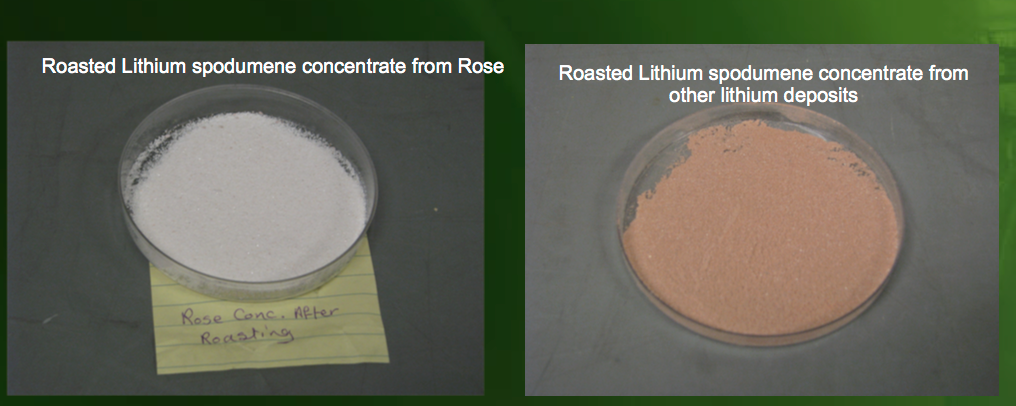

As previously mentioned, the low iron content of the spodumene concentrate produced from Rose makes the end product suitable for sale in the glass/ceramic markets.

From Critical Elements.

But of course the key highlight is that the company has been able to achieve and produce 99.98% battery grade lithium carbonate, suitable for the EV market.

Financing

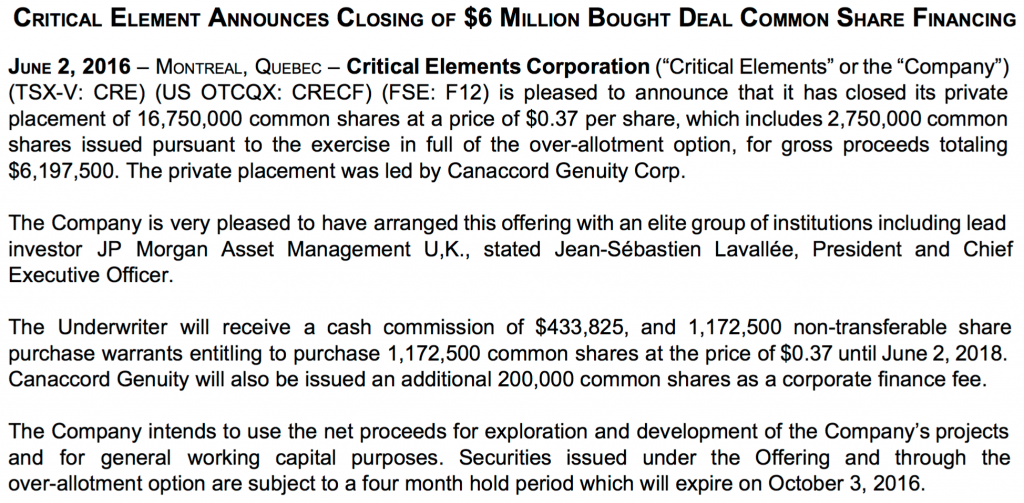

I first started buying shares of CRE.V/CRECF this past spring, prior to even more de-risking news arrived in June.

From Critical Elements.

The company was able to raise $6 million, completing a bought deal in June with “an elite group of institutions including lead investor JP Morgan Asset Management U.K.”

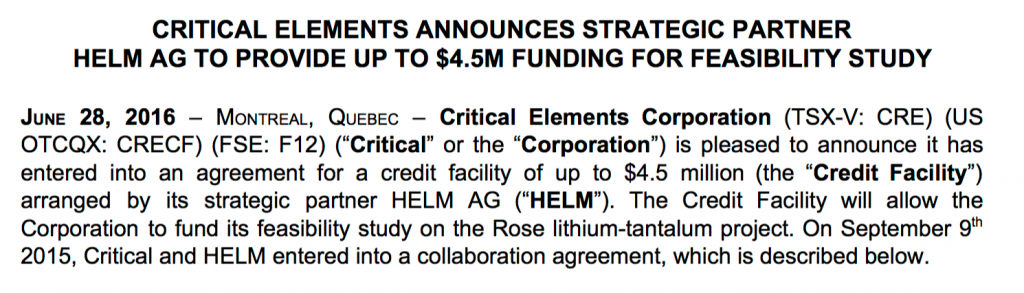

FS Financing and Mystery Partner Unveiled

Later that same month, the strategic partner finally decided to reveal itself — Helm AG.

From Critical Elements.

Just who is Helm AG, you ask?

HELM AG is a Hamburg-based family-owned company steeped in tradition and able to look back on a history spanning over 115 years. It is a multifunctional distribution company specializing in:

- Chemicals: Feedstocks and Derivatives

- Crop Protection

- Active Pharmaceutical Ingredients, Pharmaceuticals and Medical Products

- Fertilizers

When marketing our products we provide a wide range of services for our business partners.

Today HELM is one of the world’s major independent chemicals marketing enterprises with more than 100 subsidiaries, sales offices and participations in over 30 countries. Its specific local knowledge guarantees access to the major markets worldwide.

With the mystery partner, Helm AG, revealed to the markets and full funding needed to complete the Bankable Feasibility Study (BFS) in hand, I thought for certain the markets would re-rate shares of CRE.V/CRECF much higher!

How wrong I was…

But like I always emphasize on this blog, if you’re going to invest in a story, it makes a whole lot more sense to fixate on the underlying fundamentals, as opposed to the short-term price action… As we all know, Mr. Market is often irrational and illogical when we’re trying to analyze his day-to-day behavior.

This past summer, the Critical Elements was seemingly getting better and better, but the shares failed to respond at all to the “good” news…

So be it… That’s just how the game goes, sometimes oftentimes.

Peer Comparison

I previously mentioned that I thought Critical Elements provided Deep Value… But how can you know that unless you’re comparing something relative to something else? In the junior developer space, you might be wondering if there are any other candidates out there that can be used to compare with Critical Elements?

Actually there is…

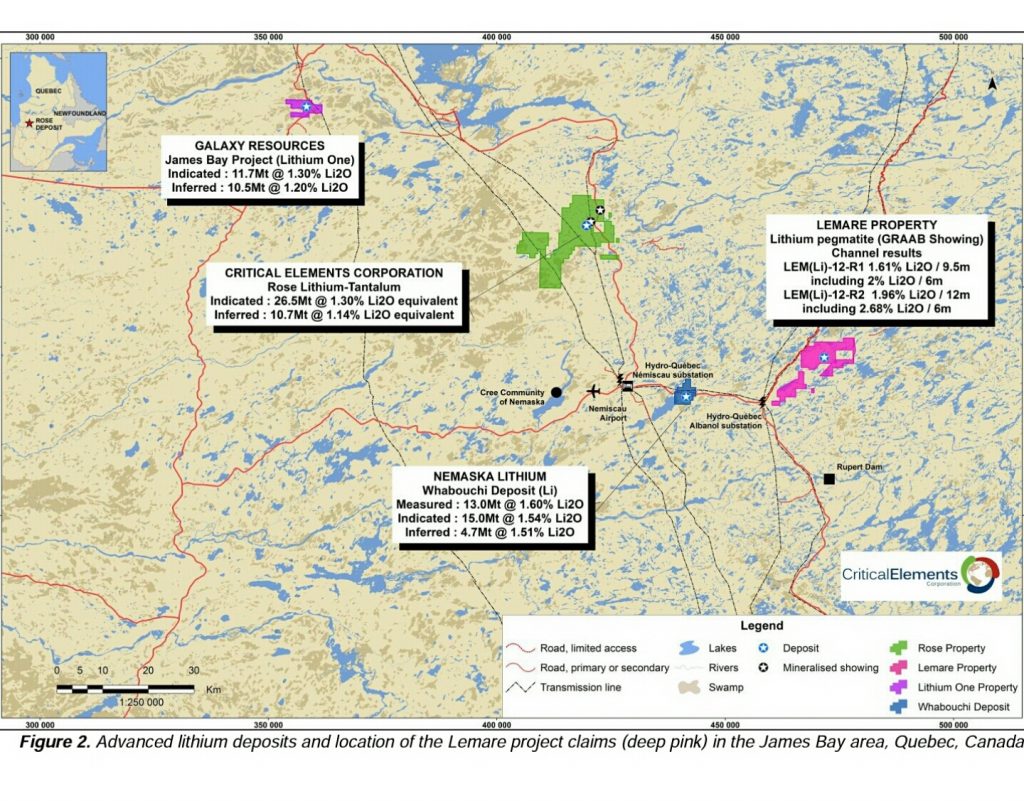

The most obvious comparison to Critical Elements is their neighbor next door, Nemaska Lithium (NMX.V/NMKEF), who also operates a hard rock project in Quebec.

From Critical Elements.

Most recent share price performance of Nemaska Lithium.

So, Nemaska is currently being valued at ~C$400 million market cap. In comparison, Critical Elements is for sale at ~C$46 million market cap.

Not quite 10x difference, but sort of close…

Is Nemaska worth the huge premium?

You be the judge.

From Nemaska Lithium.

Similar to Critical Elements, Nemaska Lithium has every intention of producing their own battery grade lithium product. However, unlike Critical Elements, Nemaska Lithium plans to focus more on cranking out lithium hydroxide (the more expensive and preferred “fuel” of companies such as Tesla), even though they will also be producing small amounts of lithium carbonate. However, Nemaska doesn’t currently have any plans to produce low iron spodumene concentrate for the glass/ceramic markets… And they have no tantalum byproduct…

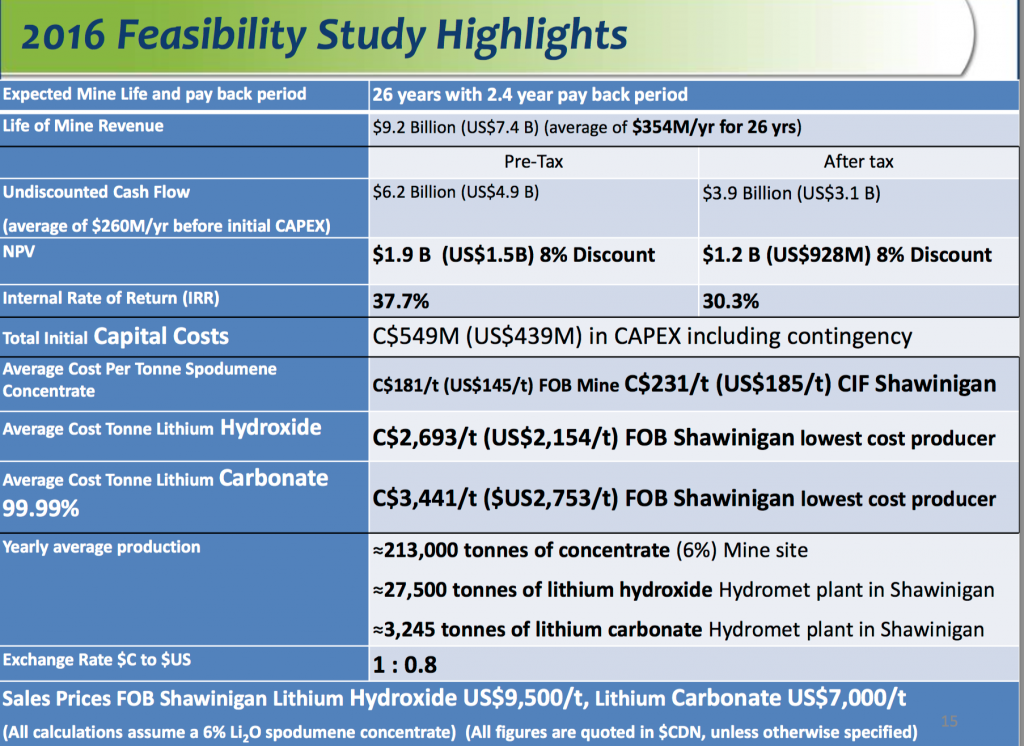

In terms of economics, Nemaska’s Whabouchi Project has has a pre-tax NPV of C$1.9 billion (after-tax of C$1.2 billion) and a pre-tax IRR of 37.7% (after-tax of 30.3%). This is all assuming a lithium hydroxide sales price of $9,500/t and lithium carbonate sales price of $7,000/t, which are very reasonable assumptions to make at this time.

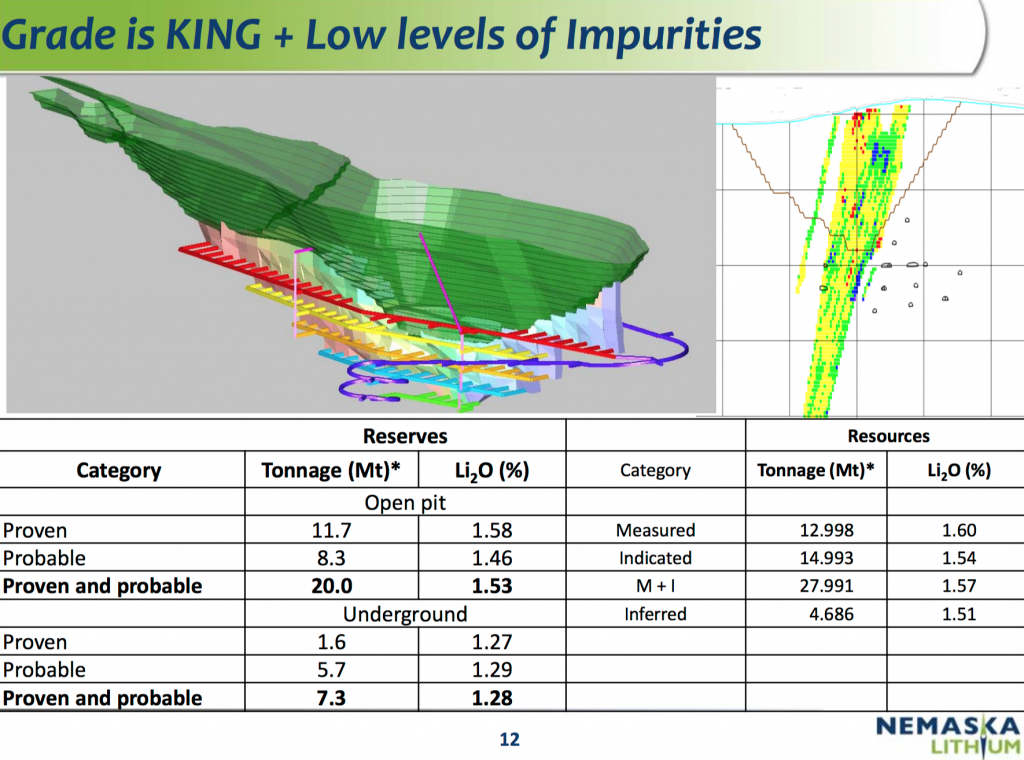

In terms of reserves and resource.

From Nemaska Lithium.

No doubt, “grade is king”, and Whabouchi is a high-grade spodumene project. In terms of size, Whabouchi has Proven and Probable reserves of 20Mt @ 1.53% Li2O (open pit), and Proven and Probable reserves of 7.3Mt @ 1.28% Li2O (underground).

In comparison, Rose hosts a current Indicated resource of 26.5Mt @ 1.30% Li2O Eq (0.98% Li2O) and 163 ppm Ta2O5 and an Inferred resource of 10.7Mt @ 1.14% Li2O Eq (0.86% Li2O) and 145 ppm Ta2O5.

Please note, at this stage of the game, we are comparing apples with oranges. Nemaska’s numbers are based off a FS completed in 2016 and Critical Elements’ numbers were derived from a much more preliminary (inaccurate) PEA from 2011.

You really can’t compare Proven and Probable Reserves to Indicated and Inferred Resources.

But more or less, the projects are of comparable scope and size… Nemaska has the edge in terms of lithium grade, but Critical Elements does get a boost thanks to its tantalum, which is what that Li2O Eq number is all about…

In terms of Life of Mine (LOM), Whabouchi is slated to be in production for 26 years, whereas Rose is projected to operate for 17 years… To me, LOM really doesn’t mean much once you’ve eclipsed the 10+ year, and/or 20Mt+ resource mark… The cash flows from the years far out into the future are so greatly discounted that they don’t impact the NPVs much at all…

Anyway, I can only work with the numbers that the companies are publicly providing to help me draw my own conclusions, as a retail investor…

Since the spodumene from both projects are able to generate battery grade lithium carbonate/hydroxide in sufficient enough quantity for commercial production, the metallurgy/recoveries for both projects should be more than satisfactory… In terms of expenses, Critical Elements cites cash costs of $2,900/t to produce lithium carbonate, and Nemaska shows $2,154/t to produce lithium hydroxide and $2,753/t to produce lithium carbonate (only a minuscule amount of total production).

It looks like Nemaska wins in terms of cash costs… But also keep in mind that initial CAPEX for Whabouchi is $439 million, whereas Rose is currently projecting somewhere ~$270 million.

Nevertheless, when we are talking about the current spot price of lithium carbonate and lithium hydroxide selling for well north of $10,000/t, there’s plenty of profit margin to be found at both projects…

Share Structure

When comparing mining companies, an important, but underrated metric to use is to look at the share structure of each company.

From Critical Elements.

On a fully diluted basis, Critical Elements has 153 million shares and a market cap of C$61.2 million.

From Nemaska Lithium.

In comparison, on a fully diluted basis, Nemaska has close to 400 million shares and a market cap of C$571 million. Many of those options and warrants are currently very much in the money…

Although at times underappreciated by some investors, much credit needs to be given to Critical Elements’ management team for being so disciplined and able to maintain such a tight share structure, particularly in spite of a most brutal bear market in commodities experienced these last 4-5 years…

When it comes to juniors, most management teams have no qualms about diluting their shareholders into oblivion… Anytime I can find a company with a tight share structure, I am most grateful!

Peer Comparison Summary

As you can see, this comparison game can go on indefinitely, and with enough time and effort I’m sure you’ll be able to find pros/cons for each project…

When it comes down to it, I feel like the huge valuation gap that exists between the two companies primarily comes down to this:

- Nemaska has a FS completed as recently as 2016, whereas Critical Elements only has an outdated PEA from 2011 (FS is in currently in progress and expectations are for completion sometime in Q1 2017?).

- Nemaska has an offtake agreement with Johnson Matthey and has already received $6 million in a first installment payment, whereas Critical Elements has a take-or-pay offtake agreement with Helm AG but one that won’t be executed until after the FS is completed.

- Nemaska’s Whabouchi mine is fully permitted and entering into the financing/mine and plant construction stage of the game. Coupled with the two bullet points above, Nemaska is seen by the market as being further ahead than Critical Elements and closer to production.

- Nemaska is much more heavily touted and advertised through promos, newsletters, media, etc., whereas Critical Elements is an obscure, unknown entity in the lithium space. One could even argue that the management team at Critical Elements is too focused on the “grunt work”, and not enough on marketing… Critical Elements doesn’t even have an Investors Relations (IR) person on staff for crying out loud… They currently outsource IR work to Paradox Public Relation… And I’m speculating, but I would imagine that shares might be trading quite a bit higher if the company was called “Critical Lithium”, instead…

With all that said, bottom line — Is Nemaska worth ~9x premium (in terms of market cap not enterprise value) to Critical Elements?

I dunno… that’s up for you to decide.

Based on my own research and due diligence, I’m inclined to say “no”… Which explains why I’ve “backed up the truck” with CRE.V/CRECF shares, and why I ultimately decided to part ways with my shares of NMKEF.

Make no mistake about it, there is no doubt in my mind that Nemaska and its Whabouchi project are high quality, I just can’t rationalize paying that much more for a company, though, when I can buy shares of its next door neighbor for significantly less… And some investors would even argue that Nemaska is a riskier project since they are trying to get into production using a patented process (unproven on a commercial scale) to produce lithium hydroxide… Ultimately, Nemaska may prove to be massively successful, but when you need to construct a Phase 1 plant first to demonstrate proof of concept, there are indeed risks/uncertainty involved…

Just sayin’…

Anyway, in my eyes, the market has is all wrong right now — Either Critical Elements is severely undervalued, or Nemaska is significantly overvalued…

If the “truth” lies somewhere in-between? Sure, I’ll be plenty happy to take the “re-rating”! In any case, we’re talking about Deep Value when it comes to Critical Elements.

Resisting Temptation

When it comes to junior mining stocks, particularly when we are talking about a HOT sector like lithium (yes, I realize it’s COLD right now, but it will come roaring back at some point), it’s easy to give in to temptation and chase momentum upwards…

I would highly caution against doing this… It can (and does) end in tears for investors!

Check out Alset Energy (ION.V) and its most recent rise to stardom and plunge back into the darkened abyss…

By no means am I trying to single out any one company, but the above just goes to show what can happen when you’re out “chasing the hot ticket”, and more focused on GREED than solid fundamentals.

Just check out the share price performance of this latest “hot shot” in lithium land.

That’s right, shares of Millennial Lithium (ML.V) are up a staggering 2,088% in the last six months alone!

Again, I’m not hating, but if we tune out the noise, what do we have here, exactly?

- Strong evidence to suggest a world-class lithium deposit is in the making in terms of size, grade, infrastructure, economics, time to money/production?

- Defined resource?

- PEA?

- FS?

- Offtake agreement?

- Etc.

Here’s their latest Millennial Lithium Corporate Presentation… You tell me what you find on there… I’m definitely not seeing much that gets me excited enough to pay that steep of a price for shares, though, that’s for sure…

Wrapping Up

As for me, I’m sticking to a more “boring” development-stage story… No, perhaps Critical Elements doesn’t have “blue sky potential”, which is what momentum traders are all after, but at the current price, I can’t seem to locate a better deal in lithium stocks…

I mean that wholeheartedly, despite the most abysmal share price performance of late.

*Yawn*

Nothing to see there… Unless I get word that Critical Elements is abandoning the Rose project due to a terrible FS, or Helm AG is pulling out altogether and not moving forward with the take-or-pay contract, it’s just business as usual…

Moving along…

I often get accused of being nothing more than a “wild gambler” who doesn’t know how to invest… But I’m also that same guy who can tune out day-to-day price action noise and focus on the Bigger Picture… I’m not trying to day trade these shares, much less even attempt to swing trade them frequently… As I’ve stated many times before, when it comes to lithium stocks, my intentions are to hold for about 3-5 years, unless the gains that I’m looking for come even sooner than that…

With clean energy and EVs, yes, I do see a paradigm shift and massive revolution that will change the world forever… I’m guessing around 2018-2020 is when these stocks will peak, so I’m hopping onboard the Hyper-Growth train… And with a company like Critical Elements, I feel like right now I’m able to locate both Hyper-Growth and Deep Value.

Although entirely too lengthy, I hope this post clearly explains to readers as to why Critical Elements is currently the third largest position in my mining portfolio!

But as always, please do your own due diligence and conduct your own research before making any kind of financial decision! I will NEVER recommend you to do anything with your own money!

Also, I would highly encourage anyone interest in lithium stocks and the Critical Elements story to please watch those two videos that I shared above. They are well worth your time…

And if you have serious interest and really want to learn as much as you can, I would recommend you head on over to Stockhouse and join the CRE forum! Even I’m on there (FI Fighter). There, you will get to meet and interact with the most informed CRE enthusiasts…

Bonus Material

Even Jim Mellon (aka the Warren Buffett of the UK) likes Critical Elements!

Check out the 42:10 mark and 49:45 mark of the following video… Thanks to Blaggers (Stockhouse) for this important post!

Fight On!

I picked up crecf at .43 and several other miners back in May. Haven’t been keeping up with lithium, thanks for the update and insight. I added more shares yesterday and lowered my cost average to .39 now at 60k shares. I’m waiting to see if it goes lower before buying more.

JC,

You bet! That’s a great cost basis and long-term you should come out well ahead.

All the best!

Thanks for the update - going to read through when I have some time!

Adrian,

Sure thing! Take your time and I highly recommend you tune in to those video presentations with management as well.

Cheers!

Awesome write up man. Always appreciate your posts like this - you make it very easy to follow along. I’m still down on most of my picks becausce I averaged in since Spring until now with some buys in August. Only wish I got in sooner 🙁

Need more cash to use in uranium and lithium. I do have a bunch tied up in Otis Gold Corp - waiting on pending assays from “Crab Claw” which may move it higher… hoping for a double or more to redeploy into these.

Adrian,

Thanks for the kind words, I appreciate it.

Lots of folks anxious for the drill results of OOO, fingers crossed and best of luck on hitting some high grades!

Happy hunting!

Nice article, love your site!

I’m curious about what stock exchange you would prefer for buying shares?

TSX, FSE, or OTC?

Would you try and buy on the exchange with the cheaper price or go with the one that is most liquid?

Thanks for the input.

Joshua,

I would go with the cheapest option available to you. If that means OTC, that should be no problem since you should be able to sell OTC directly on the TSX-V, when the time comes and you want to liquidate.

http://www.fifighter.com/precious-metals/2016/06/mining-stocks-why-you-should-not-fixate-on-the-otc-markets/

Schwab One is a terrific trading account for TSX, TSX-V listed stocks since their online system automates the buying/selling process to give you the default best price between those exchanges and the OTC.

Cheers!

[…] is my favorite idea in lithium right now because the current valuation is an absolute joke (relative to its peers and potential NPV of its […]

Jay you have done an amazing job with this analysis!! Your rock man!! I have been following your blog for a couple of months now and have been waiting for your analysis of CRE for a while now (I discovered your blog through StockHouse).

I am new to the mining world and reading this blog has been extremely helpful..

I am also very bullish on CRE, once the BFS is released the Market Cap should be anywhere between 10% to 50% of the new NPV. let’s hope for the best..

Good luck to all of us and thank you very much for the great work you are accomplishing in this blog.

PS : Do you mind if I share the link to this page on CRE’s Bullboard on SH? I really think that they will enjoy it..

Cheers!

Karoo,

Thanks for the kind words, I’m glad you enjoyed the article. Absolutely, feel free to share the article, although I’m sure it’ll just read like I’m preaching to the choir for those Stockhouse guys… In fact, I got most of my education on CRE from those fine folks over there 😉

Yup, just anxiously awaiting the BFS now and hopefully with those results out and the Helm offtake officially signed and cemented we can see the stock re-rated to at least align with CRE’s peer group, if not at a slightly higher premium since we’ll be on the fast track to production with financing/mine construction as the next steps, which is a lot further along than where most lithium juniors are with their projects.

All the best!

Hey,

I really like your writing and appreciate your thoughts. I agree with the EV revolution but I have concerns about lithium. Is lithium the best bet to benefit from this hyper-growth story? What if lithium becomes useless in batteries (because some other technology and material)? I think that the battery technology is the bottleneck that prevent EVs from becoming more common. And if Lithium ion batteries can advance about 5% in year I think its only a matter of time that some other technology passes lithium-ion batteries.

I know that most of these are only early stage stories but there is so many ideas being developed that it is little worrying (http://www.pocket-lint.com/news/130380-future-batteries-coming-soon-charge-in-seconds-last-months-and-power-over-the-air).

Also Fisker trying to challenge Tesla with graphene super capacitors and have plans to start producing as soon as 2017 http://www.businessinsider.com/henrik-fisker-is-using-revolutionary-battery-tech-for-electric-car-2016-10?r=US&IR=T&IR=T

I have about 5% of my portfolio in Critical Elements and I´m planning to start a position in Birimian Limited also. My investment idea is as you have written in this blog post, the peak in 2018-2020.

How do you see the advancements in battery technology? How possible it is according to you that we will see a breakthrough in some other technology before the peak in lithium (2018-2020)?

And I´m not pushing the sell button because of these rumours, we have heard these for many years and still no commercial use (and I´m pretty sure we don’t see graphene supercapacitor Fisker on the streets in 2017 😉 ). Just wanted to hear your thoughts because I think you have looked into this when assessing this investment idea 🙂

TT,

Thanks for sharing the links and your thoughts. Honestly, I think lithium-ion will remain the dominant battery technology for at least the next decade, and probably a lot longer than that. Quite frankly, there are too many Gigafactories under construction and too many billions sinking into this technology for it to go away anytime soon. All these big investments will be looking for a return on their capital and everyone is moving full steam ahead with the EV revolution… Can anyone seriously imagine a company like Tesla swapping out of lithium-ion and experimenting with some new technology right now? Highly, unlikely… almost an impossibility in my book.

Characterizing new battery tech is no trivial task and takes many years/decades of refinement before a lab experiment can be put into full-scale commercial production. Right now, the stakes are way too high to take on that type of risk. So, I’m 1000% confident lithium-ion isn’t going away anytime soon, and I’ve placed my bets to back up my full conviction.

Graphene supercapacitors are the future, but still very far away from reality, IMHO. Even if it was viable today (fully characterized and proven to be safe and scalable), there’s no supply chain available for the amount of graphene you would need for mass adoption. Graphene is currently only being produced in minuscule quantities.

Cheers!

[…] And Critical Elements has long been a strong conviction idea of mine… […]