These days, the hype surrounding electric vehicles (EV) is rapidly growing, and naturally, you’re going to have your skeptics and doubters. There ain’t nothing wrong with that. Since I’m new to the space myself, I’ve been spending a lot of time reading articles, forums, research papers, etc., trying to learn more so that I can better understand the industry. As readers should be well aware by now, for the most part, I don’t like to write about topics that I know absolutely nothing about… If I do, then at least I’m open and honest with myself, admitting that I’m still very much a newbie and still learning as I go… For instance, I made the concluding remark as I finished up my first lithium article:

“Thanks for tuning in for this “preview” edition of my lithium updates… This update is just a “surface level” overview for anyone new to the sector… I’ll save the finer details for later, as I’m still very much learning and researching more myself… I’m still very green in this space, so it’ll take some time for me to get up to speed.”

With that said, lately, I’ve been rather amused to stumble upon so many articles on the mainstream web that are calling this rush into lithium “the latest craze”, implying that it won’t last for long, and that this “bubble” will soon burst. Again, I certainly don’t mind if someone out there disagrees with my investment thesis… Actually, I think being able to listen to as many counter-arguments and polarizing viewpoints as possible is the most beneficial thing one can do to firm up their own thesis…

Unfortunately, when it comes to lithium, I have so far been wildly unsuccessful in my attempts at locating any well-researched, high quality contrarian viewpoints.

Instead, what I’m finding are some rather lazy, lazy, lazy articles out there…

It’s All Hype?

Anytime we have the start of a new mania, the first thing many people are going to want to do is throw caution to the wind. That happened when the internet was first gaining ground (see the title image of this article), when the first smartphones were released (really, who want to walk around with a personal computer in their pockets?!? And a phone that doubles as a digital camera? Capacitive touch screen? That’s so lame and gimmicky! I need a keypad to type!), and now with electric vehicles (the range sucks and charging takes FOREVER, it will never catch on).

When it comes to lithium, the critics will hastily want to compare the sharp rise in some of these mining stocks to the dot-com bust, because… well, that’s the easy and convenient thing to do… In their minds, “Hey, here’s something that shot up really fast, so, umm, it must be artificial and purely hype-driven… But why I should I bother researching fundamentals? I’m just gonna tell all my readers that this thing is just a fad and that it will fade away shortly…”

Here’s the latest article that more or less attempts to discredit the lithium boom…

Should you bet big on these ASX-listed lithium shares?

Here are some snippets of The Motley Fool article, linked above:

The Motley Fool:

“As prices rise, more and more explorers will venture into the sector in search of lucrative returns, which will increase the market’s supply. When that happens, prices will likely begin to decrease which will wreak havoc for those companies who have either overpaid for acquisitions or maintain higher costs than their competitors.”

My Response:

Let’s look at the supply and demand fundamentals before jumping to any conclusions…

Supply and Demand

Anytime you have a major disruption, or paradigm shift in an industry, you will ALWAYS have start-up companies emerging onto the scene hoping to come up with the next “killer app”. After the iPhone was first released in 2007, pretty soon everyone and their grandma wanted to write software applications for it. Angry Birds, Yelp, Uber, Lyft, Instagram, Facebook, Twitter, etc., etc., etc, just to name a few of the millions of apps out there… As for the hardware manufacturers? You had Blackberry, Samsung, Nokia, LG, HTC, etc. betting BIG on this latest revolution, this company called Google (you might have heard of them) launching this thing called Android to compete directly with iOS, and a bunch of brand new Chinese companies like Xiaomi (who?) get into the fray, trying hard to initially earn even just a tiny morsel of an enormous (and rapidly growing) pie.

Would you have in 2009 deemed that the app space was already far too overcrowded and doomed for failure? Ditto for hardware? Does anyone, even now (almost a decade since the first iPhone got rolling), think that mobile is completely tapped out and the there are no more big bucks to be made?

I seriously doubt it…

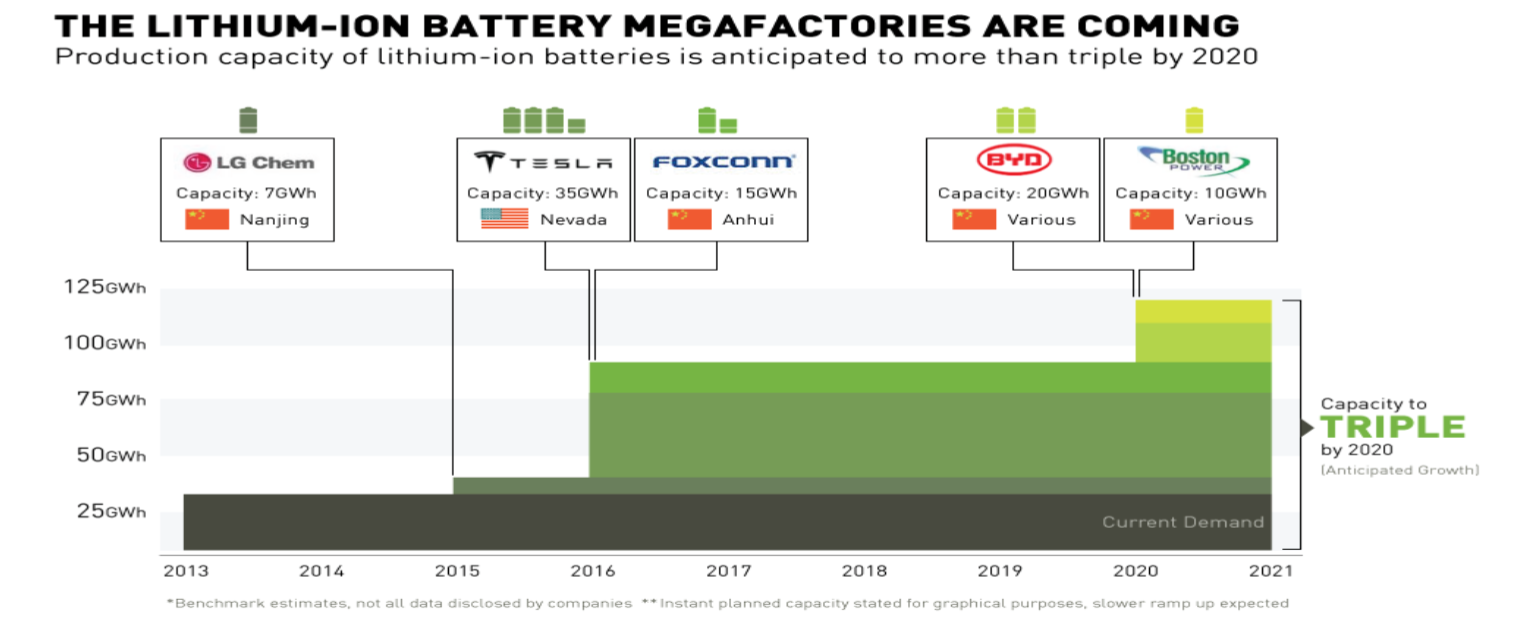

When it comes to EVs and lithium, why should it be any different? Everyone can see the Megafactories coming from 100 miles away, and at this stage of the game, it’s far too late to try and stop them.

From Nemaska Lithium:

Lithium-ion Megafactories:

- LG Chem (capacity 7 GWh)

- Tesla (capacity 35 GWh)

- Foxconn (capacity 15 GWh)

- BYD (capacity 20 GWh)

- Boston Power (10 GWh)

The production of lithium-ion batteries is expected to triple by the year 2020… which in turn is going to require a ton more lithium supply.

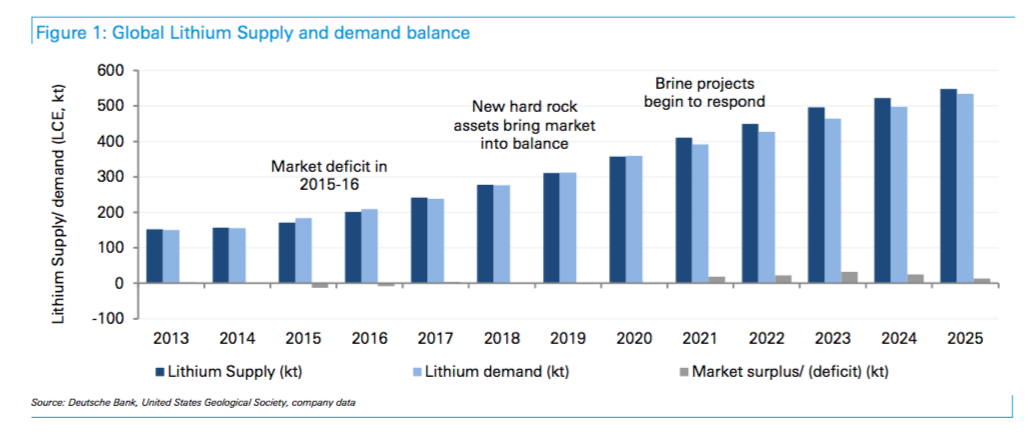

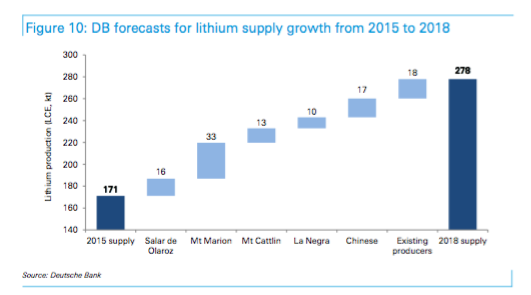

Global lithium supply and demand chart — Demand of 181,000t Lithium Carbonate Equivalent (LCE) in 2015 is expected to grow to 535,000t LCE by 2025.

As shown by Deutsche Bank in the image above, the global lithium market was already in a supply deficit in 2015 and is due to operate in one again in 2016. Perhaps that explains why the Chinese are more than willing to pay upwards of $20,000+/t for lithium carbonate these days… According to the chart above, the supply crunch trend should continue into 2017 (just slightly), but by 2018-2020, the supply/demand dynamics should be more or less on parity with each other, due to the fresh incoming supply of new lithium resources.

Here are the projects that are currently under development or just ramping up to nameplate capacity.

1) Orocobre Limited (Salar de Olaroz) - Brine in Argentina. Operational and in production.

Nameplate capacity is 17,500 tonnes per annum (tpa) of LCE production during Stage 1. The company has had “bottleneck” issues with commissioning since 2015, and is projecting that it won’t be up to speed until September of this year.

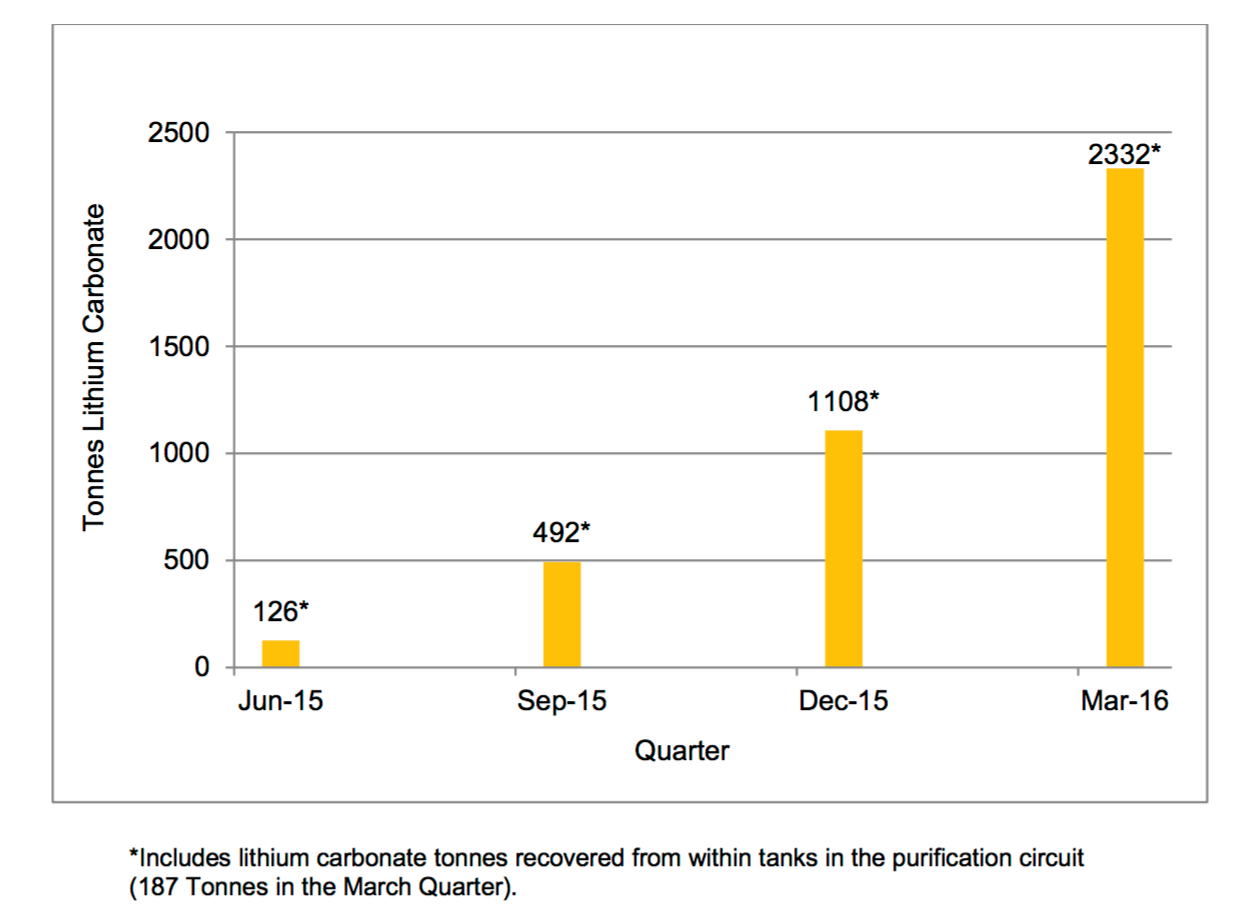

Latest quarter (March 2016) production of 2,332t LCE. Orocobre still has a long ways to go to get up to nameplate…

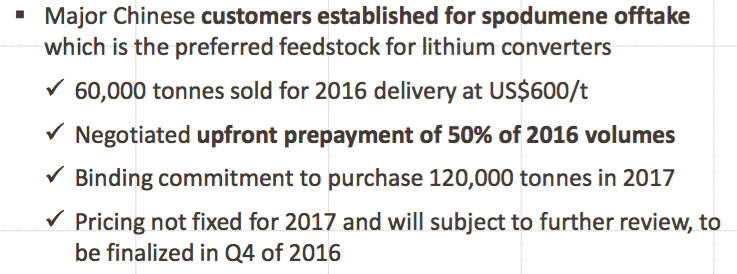

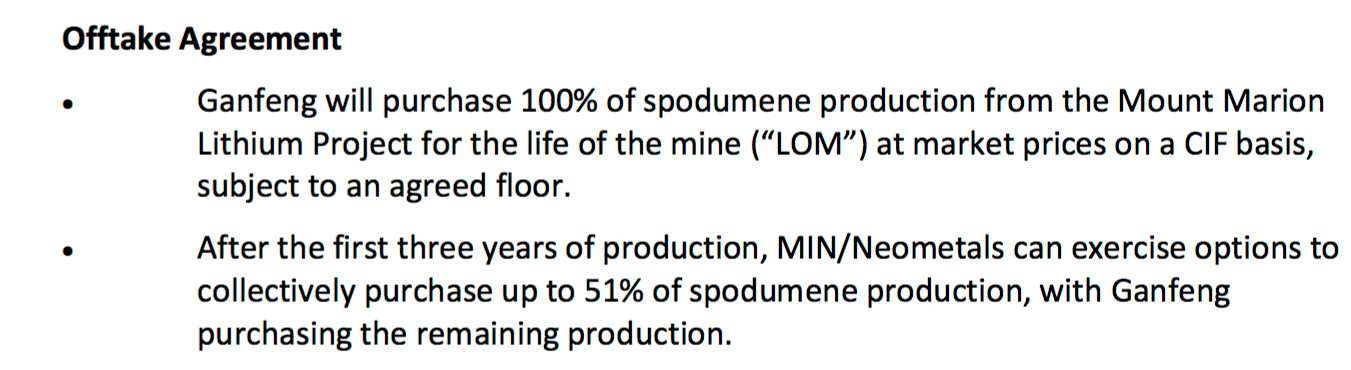

2) Ganfeng Lithium, Mineral Resources, and Neometals (Mt. Marion) - Spodumene in Western Australia. JV (43.1% Ganging Lithium; 30% Mineral Resources - operator; 26.9% Neometals). Currently under construction (commissioning in June/July 2016).

Expected to produce around 27,000tpa of LCE. Scope for flotation circuit to further increase production. Offtake partner is Ganfeng, who will initially purchase 100% of spodumene produced from Mt. Marion. After 3 years, Neometals and Mineral Resources have the option to purchase up to 51% of the spodumene concentrate, with Ganging retaining the right to purchase the remaining 49% of production.

For 2016, production is expected in the order of ~6,100t of LCE.

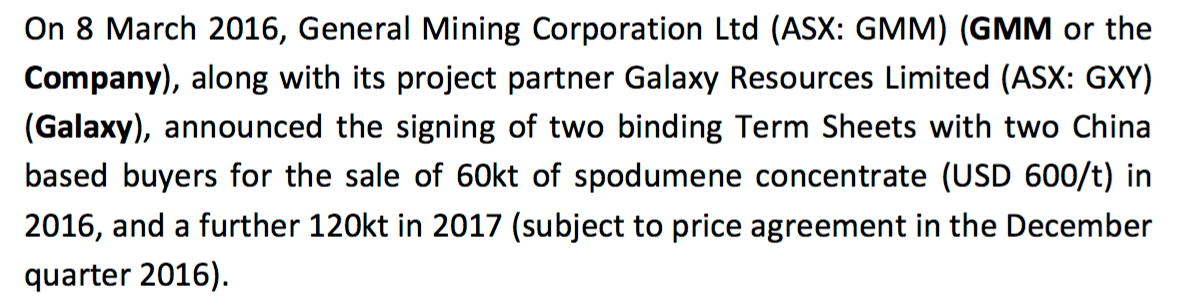

3) Galaxy Resources and General Mining (Mt. Cattlin) - Spodumene in Western Australia. JV (50% Galaxy Resources; 50% General Mining). Re-commenced production in March 2016.

Mt. Cattlin is an operating mine that was previously put on Care and Maintenance in 2012 due to poor recoveries and a depressed lithium market. According to the Deutsche Bank report, Mt. Cattlin should eventually produce 13,000tpa of LCE, when it is running at capacity.

For 2016, production is expected in the order of ~3,300t of LCE.

Mt. Cattlin is a relatively modest-sized spodumene mine, but it is currently in production and both partners, Galaxy Resources and General Mining, have secured an offtake agreement with numerous Chinese companies.

4) Albemarle (La Negra) - Brine in Chile. Operational and in production.

Albemarle is one of the “Big 3” lithium producers, currently responsible for ~15% of worldwide production. Albemarle operates the world-class Salar de Atacama project, the largest salt flat in Chile that is home to 27% of the world’s lithium reserve base.

Albemarle owns the La Negra processing plant in Antofagasta, which has been in operation since 1984.

Most recently, in February 2016, Albemarle was granted a permit from the Chilean government to allow for increased annual production, due to growing consumer demand.

The MOU provides Albemarle with sufficient lithium to support the production, over a 27-year period, of 70,000 MT annually of technical and battery grade lithium carbonate and 6,000 MT annually of lithium chloride at Albemarle’s two manufacturing facilities in La Negra, Antofagasta, as well as at a third lithium carbonate facility that Albemarle will commit to construct under the MOU.

5) and 6) Chinese and Existing Producers

Lastly, we can expect to see new supply coming online from the Chinese and other lithium producers, which according to Deutsche Bank’s research report, should account for an additional 35,000t of LCE between now and 2018. In total, supply should increase from 171,000t of LCE in 2015 to 278,000t of LCE by 2018.

In general, China is a very opaque market, so I am not going to even bother trying to dig into their details; For a medium-term (3-5 years) horizon, I will simply rely on the ballpark number provided by Deutsche Bank as being reasonable assumptions for China’s future lithium output.

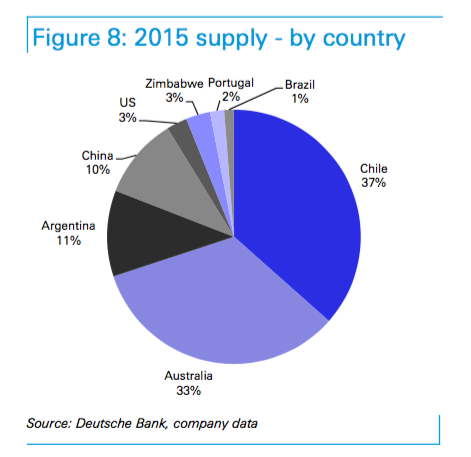

Big picture, China is not a major producer of lithium, anyway. China’s 2015 lithium production only accounted for 10% of worldwide supply.

To my knowledge, I do not yet have any reason to believe that China has the near-term domestic capability to oversaturate the markets with a fresh supply of lithium (whether from spodumene or brine sources), like they had done previously before with other natural resources such as coal, graphite, rare earths, etc.

As far as I can tell, China is merely a strong buyer (not producer) of lithium… And you guys know me, I like to try and invest where I think Big Money is headed towards next…

Thoughts

As shown above, much of the new production coming online between now and 2018 will come from Salar de Olaroz, Mt. Marion, and Mt. Cattlin. No doubt, some ramp up time will be required and “teething” issues will need to be resolved before nameplate capacity can be reached.

If Orocobre is to be used as an example, getting a new project up and running smoothly is NOT a trivial matter! Brine projects, in particular, are especially NOT EASY!

From Mr. Lithium, Joe Lowry:

$ORE continues to under perform in volume and quality. The longest “start-up” in #lithium history drags on. pic.twitter.com/DDKYj3gDHg

— Joe Lowry (@globallithium) April 28, 2016

Many of these junior brine explorers with “pie in the sky” dreams of striking it rich and supplying lithium to Tesla by 2020 will soon themselves find out the hard way… As will their investors. Realistically, it’s just NOT going to happen…

Orocobre completed their Definitive Feasibility Study (DFS) for Olaroz in May 2011…

It’s now been over 5 years since the DFS, and Olaroz still hasn’t achieved nameplate capacity… Orocobre is STILL sorting out “bottleneck” issues that have prevented them from getting to 17,500 tpa LCE.

Do these grassroots junior exploration companies (who don’t even have a Preliminary Economic Assessment completed yet, let alone DFS) really think that they’ll be able to catch Tesla on time for the Model 3 launch and ramp up (2018-2020)?!?

Yes, it’s nice to have BIG aspirations, but who are we trying to fool here? I don’t care if you’ve negotiated a “supply agreement” with Tesla, in advance… When the appropriate time comes and Tesla needs a REAL SUPPLY of lithium, they will turn to the select few companies (mostly the majors) who can actually produce the stuff in any kind of meaningful quantity.

Anyway, there should be no assumptions made that a surplus of new lithium will soon flood and overwhelm the world’s lithium supply chain. From now until 2018, there are only a handful of new projects that are slated to come online (ONLY from 6 sources, according to Deutsche Bank).

Please Note: To my knowledge, there are also some advanced-staged stories coming out of Quebec that should be ready for commercial production sometime in 2018-2019. In particular, Nemaska Lithium (NMX.V) and Critical Elements (CRE.V), both spodumene projects.

Nevertheless, the supply and demand plot shows that supply and demand will start to find an equilibrium at ~300,000t of LCE, around 2019-2020.

Though almost certainly, there will NOT be a million new projects coming out of the woodwork to oversaturate the markets, contrary to what some “lithium bears” might be suggesting…

With so many Megafactories being built across the globe, there is no doubt that there is going to be a mad rush from battery and chemical manufacturers to secure any kind of offtake agreements that are available. Quite frankly, at least until after 2020, it’s going to be extremely slim pickens for those in need of LCE supply.

Don’t Underestimate Disruptive Technology

During the early stages of a paradigm shift, analysts, researchers, laymans, and just about everyone else will ALWAYS underestimate demand to the downside of things. That’s just human nature… Remember, once upon a time, people scoffed at the notion that anyone would want to carry a “bulky personal computer” in their pockets… Well, the smartphone revolution arrived in 2007, and blew away most everyone’s expectations by 2016…

Even when the Model S first arrived on the scene, many skeptics were dubious that it would ever amount to anything more than an expensive science project… But when Consumer Reports called the Model S the best car that it had ever tested, and later, the Model S P85D scored a 103 Out Of 100, more and more people became true believers.

With the EV revolution, my gut feeling is that just like with the smartphone and internet before it, this major disruption will be off the charts and one for the record books.

This time around, Tesla is the flash (like Apple before it), but China will again remain the substance that drives the real, substantial growth (at least in my mind).

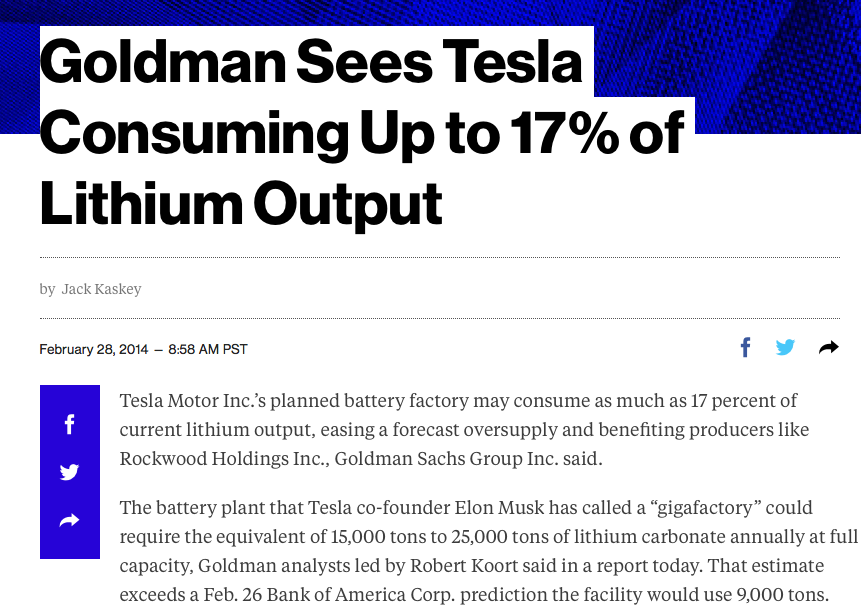

But as it pertains to Tesla, Goldman Sachs sees the Tesla Gigafactory alone requiring between 15,000-25,000t of LCE annually to operate at full capacity.

Here are statements made on the Tesla Gigafactory website, addressing future demand requirements for its massive Reno facility.

“Tesla broke ground on the Gigafactory in June 2014 outside Sparks, Nevada, and we expect to begin cell production in 2017. By 2020, the Gigafactory will reach full capacity and produce more lithium ion batteries annually than were produced worldwide in 2013.”

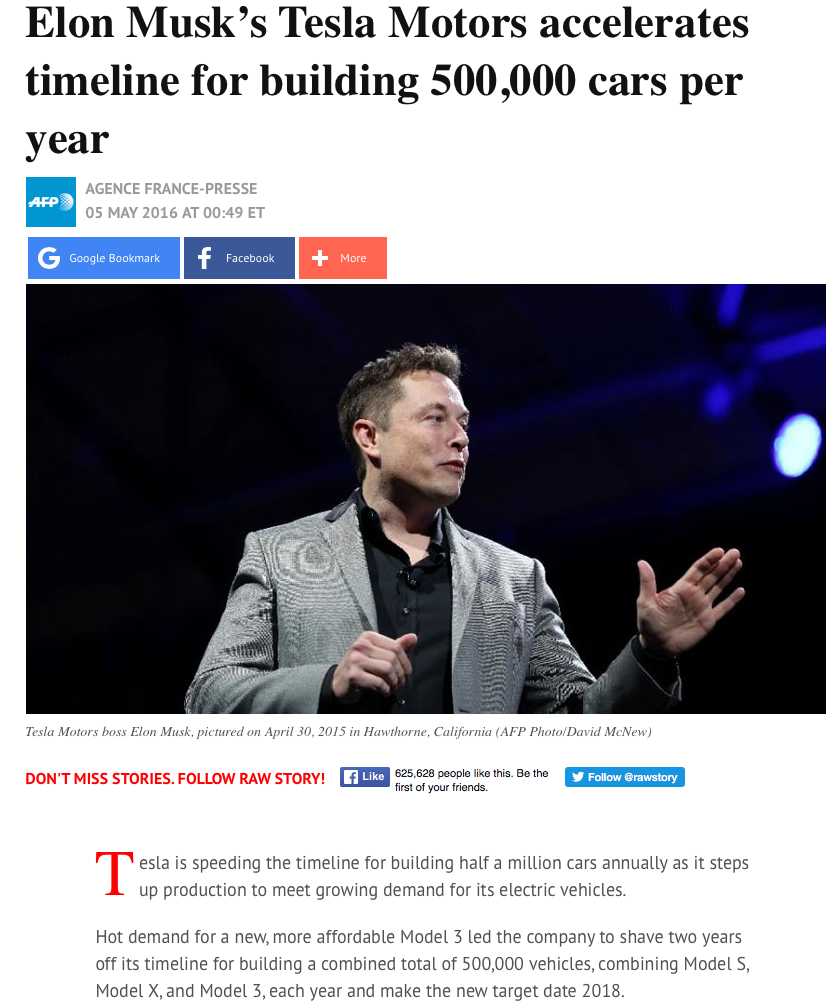

As most everyone knows by now, Tesla had recently come out and publicly stated that their goal is to get 500,000 EVs out into production per year by as early as 2018.

From RawStory:

With pre-orders for the Model 3 already eclipsing north of 400,000, the masses have spoken and let us all know that they are indeed anxious to embrace “the next big thing”.

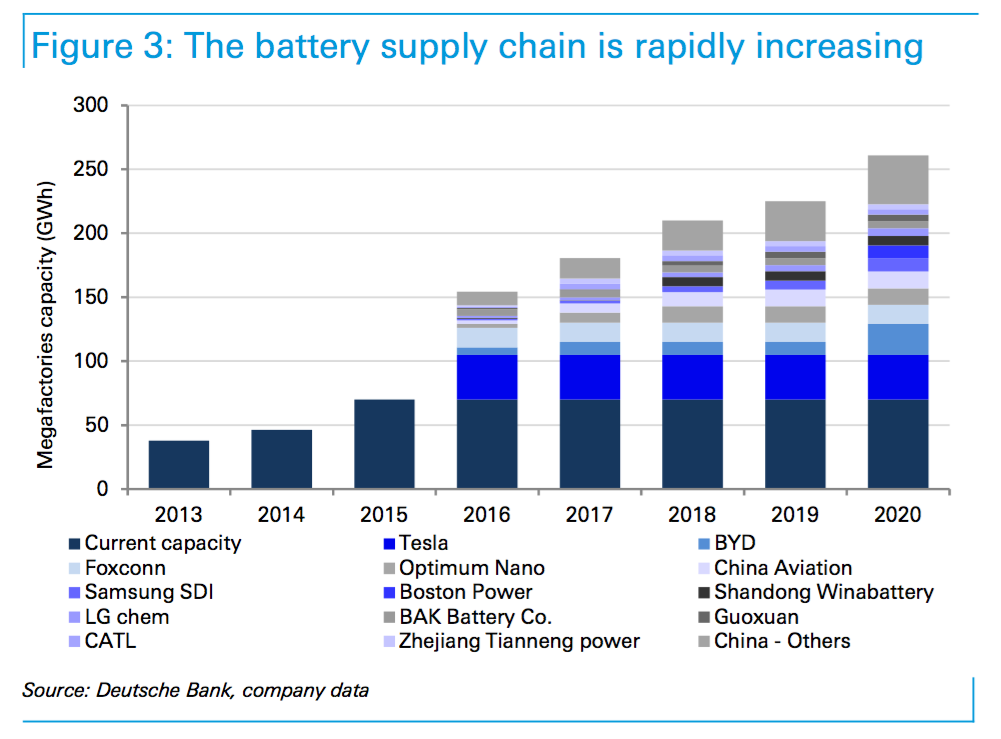

Here is how Deutsche Bank forecasts demand for batteries coming from the world’s Megafactories up to the year 2020.

In 2015, battery demand increased by 45% Year-over-Year (YoY), accounting for 40% of global lithium demand. By 2020, batteries are expected to consume 75% of global lithium demand. The above chart shows exponential growth for batteries. Further, Deutsche Bank sees about 23% Compounded Annual Growth Rate (CAGR) demand coming from EVs, up to the year 2025.

Whether Deutsche Bank’s projections ultimately prove to be accurate or way off the mark is immaterial to my medium-term (3-5 year) investment thesis… For investors, the most important takeaway from these charts and figures is the indisputable fact that the EV revolution is arriving fast and hard. As investors, we can either find a way to partake in this hyper-growth story, or we can elect to get the hell out of the way.

Regardless of what we decide to do individually, this next paradigm shift is going to happen…

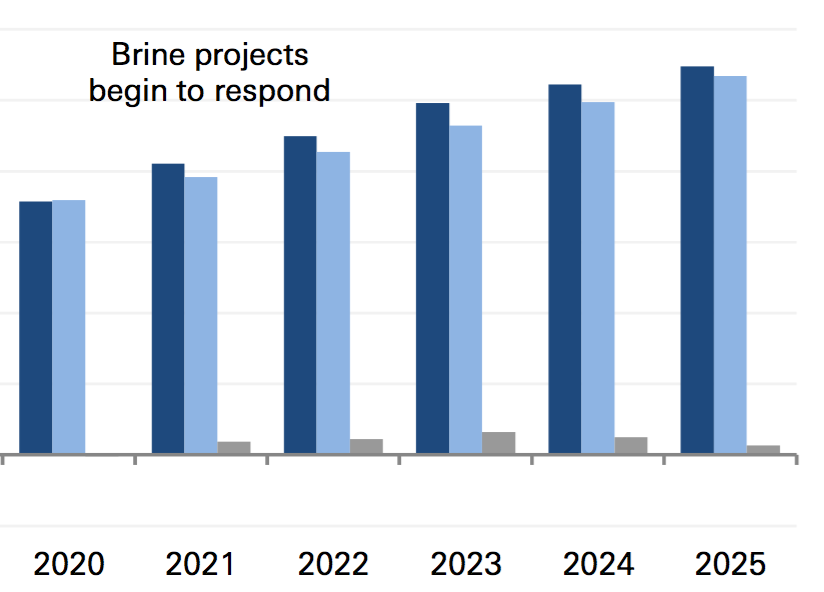

And as the chart below will show, the more sophisticated, larger-scale brine projects (that are either in exploration or development today), probably won’t be able to respond until 2020 and beyond.

So, if you’re the type of investor who is worried about “lithium being far too abundant” and it being “only a matter of time” before the price of LCE falls back to reality, you’ve got a good 3-5 year window to capitalize on the supply/demand imbalance. That would be my best guess, anyway…

Here’s what Deutsche Bank thinks.

Call me entirely too bullish, but my gut instincts have me believing that the price for lithium carbonate and lithium hydroxide aren’t going to fall off quite so rapidly, as depicted in the chart above… I just really do believe that the EV revolution will catch the world off-guard, and the demand will completely overwhelm supply over the next few years…

Experts have been off the mark (far too conservative) with disruptive technology predictions before.

From Tony Seba.

History shows us that McKinsey & Co were on the low-end with their cellphone adoption forecast by a factor of 120x… But who’s really counting?

By 2020, when the next wave of lithium projects start to make their way into production, sure, I could easily see prices for lithium carbonate and lithium hydroxide leveling off again, but still above 5 digits.

Here is where we stand in May 2016.

#lithium price update. Hydroxide selling above $28/kg in SE Asia. Some “Big 3” carbonate selling into China >$14/kg. $ALB price is lowest.

— Joe Lowry (@globallithium) May 13, 2016

After 2020, who really knows what will happen? For all we know, a company like Lithium Australia (LIT.AX) might just well have perfected their lithium extract process, bringing an unlimited supply of cheap lithium to the world. That would be a total game-changer!

For my own investment thesis, however, I should be checked out of the lithium game long before mica processing ever becomes economical… Again, 3-5 years, that’s my timeframe for this speculative trade… Probably no longer than that, unless new supply just fails to come online (for whatever reason), and/or demand ends up grossly exceeding even our wildest imaginations…

When it comes to disruptive technology, anything can happen… The sky really is the limit…

Rarely do the the stars ever align themselves so perfectly for investors, but this may indeed be the case for lithium stocks over the next 3-5 years.

But please note, nothing is for sure guaranteed! All it would take is another global economic crash, or something like another major EV fire (that grabs all the mainstream media headlines again), to impede, slow down, or temporarily halt the lithium momentum train… As always, speculate at your own risk!

More Thoughts

With all that said, I can’t help but now ask, “Does The Motley Fool author SERIOUSLY believe that any geek off the street is going to be able to buy up some random land claims in the middle of nowhere, spend 5 minutes drilling, and within a month have a fully operational, and commercially producing lithium hard-rock mine, or salar brine?”

From all accounts above, readers should be able to clearly see that there will really only be a handful of new deposits/companies slated to enter production over the next few years… And with the current spodumene projects in development, many of these companies have already entered into offtake agreements with proactive customers (who are sensing the impending supply crunch).

From Neometals.

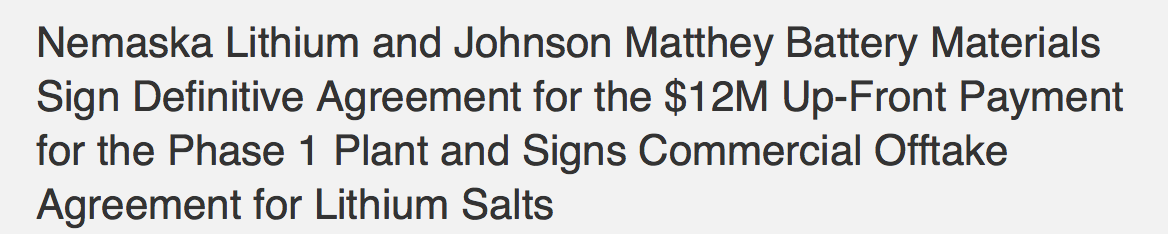

From Nemaska Lithium.

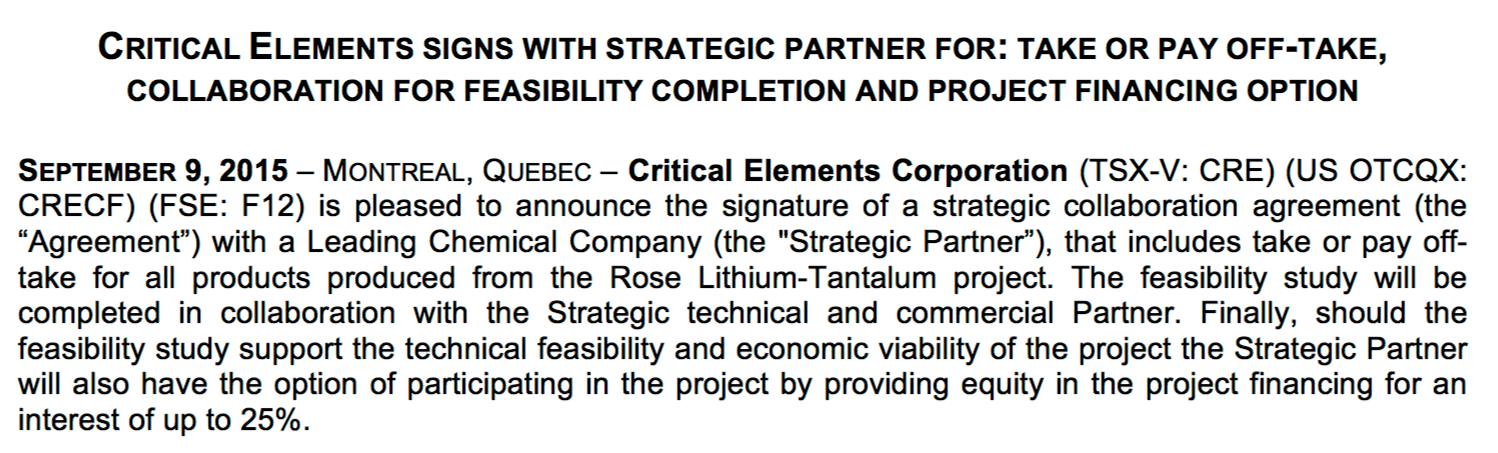

From Critical Elements.

And so on and so on…

If future supply was indeed more than abundant and so easily obtainable, would companies really go through such lengths as to commit to signing offtake agreements to ensure “100% of spodumene production… for the life of the mine…“, or make “$12M up-front payment…“, or secure “the option of participating in the project by providing equity in the project financing for an interest of up to 25%?”

I seriously doubt it…

Lastly, to address the following comments…

The Motley Fool:

“Another risk is that investors will begin to expect big gains in share prices. Shares of companies such as Prospect Resources and Altura Mining Ltd (ASX: AJM) have gained 280% and 1,500% over the last 12 months, while Dakota Minerals Ltd (ASX: DKO) has also risen 858%.”

However, those kind of returns are not sustainable in the long run. They could either slow down or fizzle out altogether, or else experience sharp falls in the event they do not live up to the hype.

To demonstrate the volatility, shares of Dakota have actually fallen 32.1% today, while Altura Mining is also down 4.1%.”

Yes, it’s true that when a sector is booming, you’re gonna have your fair share of “pretender” companies who aren’t able to offer up investors anything more than a pipe dream… Over time, those “fakers” will indeed go up in flames, it’s inevitable.

But if an investor is willing to put in the time and effort to separate out the wheat from the chaff, they’ll be left holding shares of companies who do indeed possess world class assets.

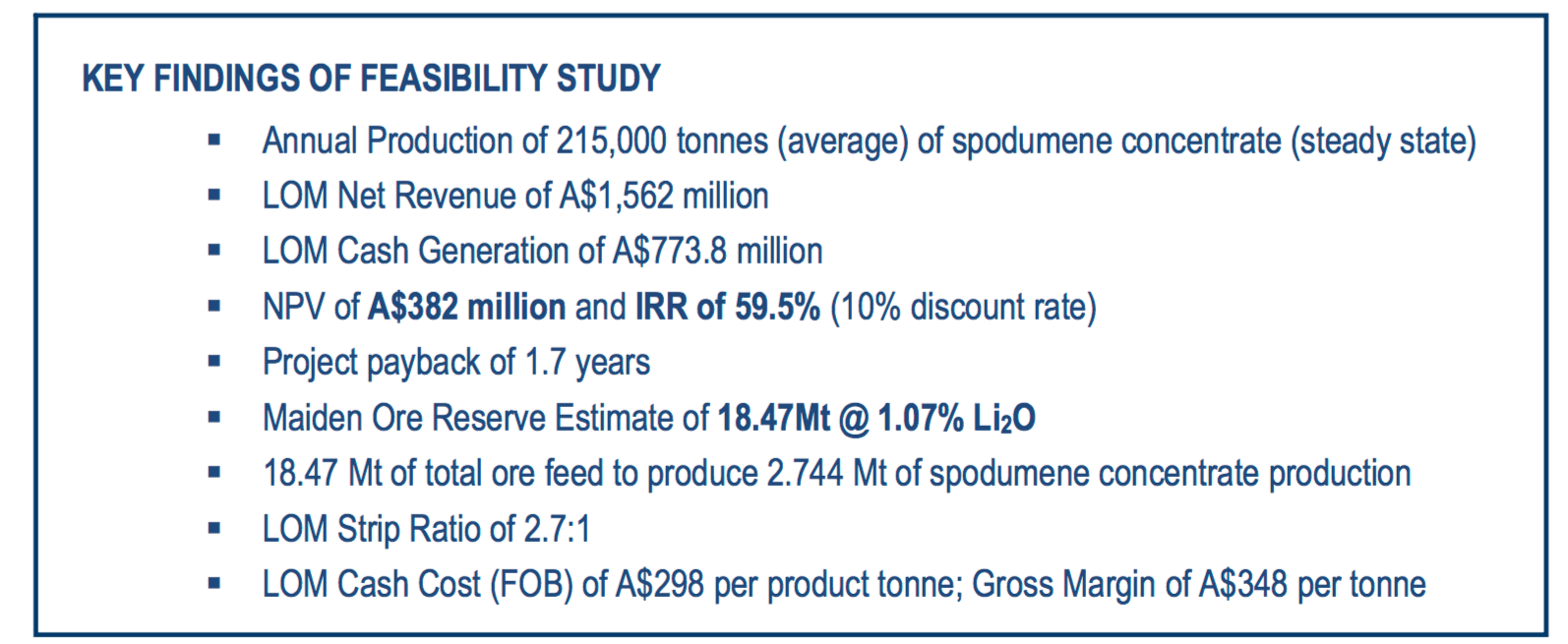

It is a gross generalization to assume that a stock is overvalued just because its share price is up (was AAPL or GOOG overpriced in 2011?). As it pertains to lithium stocks, comparing Dakota Minerals to Altura Mining would be like comparing apples to oranges. It is true, both mining companies operate out in the Pilbara region, in Western Australia, but besides that most surface-level fact, the two stories couldn’t be any more different. Dakota Minerals is an early-stage exploration company that just recently initiated its maiden drill campaign. In contrast, Altura Mining most recently completed a Feasibility Study for its Pilgangoora project in February, and is gearing up for commercial production by mid 2017.

Really, at this stage of the game, the two lithium stories couldn’t be anymore world’s apart…

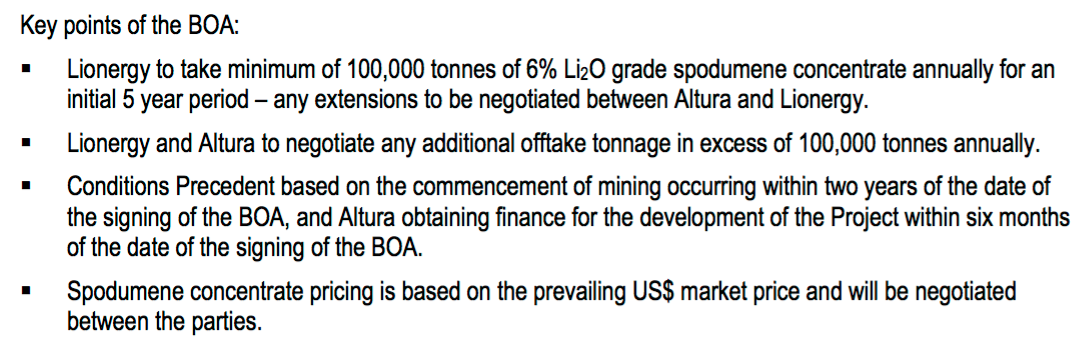

From Altura Mining:

Further, Altura Mining has completed and signed its first Binding Offtake Agreement (BOA) with Lionergy, a Chinese lithium company.

From Altura Mining.

In regards to “fair valuation”, here are some varying opinions that run contrary to The Motley Fool article’s claims that “those kind of returns are not sustainable in the long run.”

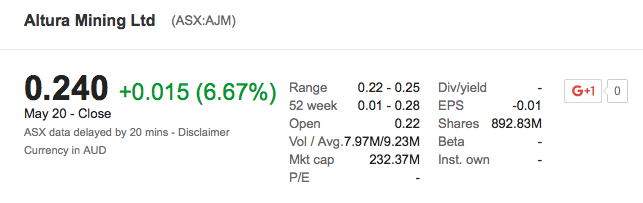

Beer and Co. Equity Research seem to think Altura’s gains are “sustainable”. In fact, they just recently increased their target to A$0.415/share, which almost amounts to a 2x increase from the May 11 AJM.AX share price of A$0.21/share.

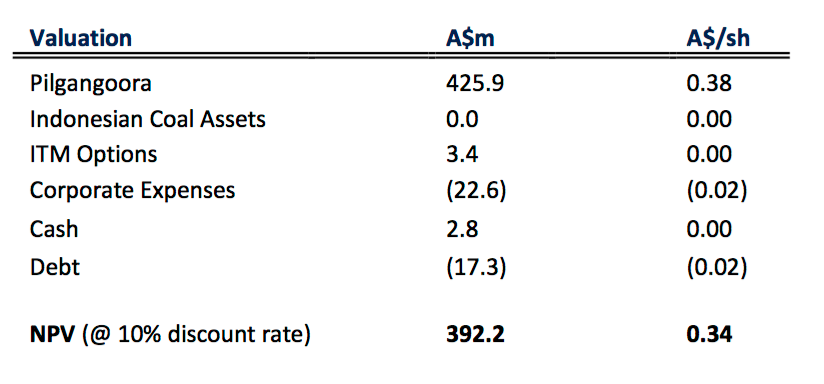

Ditto for BCP Equities, who assigned the following valuation of A$0.34/share, based on a company NPV (10% discount rate) of A$392.2 million.

Here is the current share price of AJM.AX.

The current market cap is A$232.37 million. From the Feasibility Study, the NPV (using 10% discount rate) is A$382 million, with IRR of 59.5%, assuming a spodumene market price of $494/t.

The most recent offtake agreement signed by General Mining (GMM.AX) and Galaxy Resources (GXY.AX) with Chinese buyers show that spodumene prices are being settled at $600/t.

Should spodumene prices stay flat at $600/t, or continue to trend up from this point moving forward, the economics for Altura Mining’s Pilgangoora project will actually improve from the already robust figures that the FS is currently showing. In other words, it would not be far-fetched, or unrealistic to assume that shares of AJM.AX will continue to go up from here, despite the fact that the stock is already up over 1,000% Y/Y.

For lithium companies who will be producing the final end products (lithium carbonate and lithium hydroxide) themselves, you might find the following valuation.

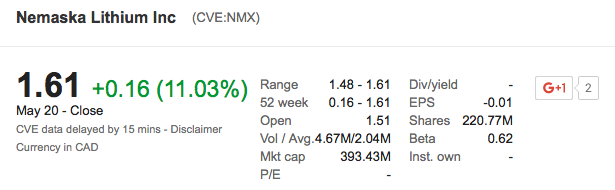

NMX.V is currently trading at C$1.61/share, or C$393.43 million market cap.

The 2016 Feasibility Study shows the following economics.

The after-tax NPV (8% discount rate) is C$1.2 billion, and after-tax IRR is 30.3%, assuming a lithium hydroxide sales price of $9,500/t and lithium carbonate price of $7,000/t. As previously mentioned, both lithium hydroxide and lithium carbonate are currently selling for north of $10,000/t in China. Obviously, the NPV and IRR using today’s lithium prices would be even higher than that shown in the above chart.

With that said, are shares of NMX.V currently overvalued?

Maybe, maybe not…

So, I’m just going to conclude by saying, “Do your own due diligence before forming any definitive conclusions.”

As an investor who is constantly trying to learn and get more and more educated, I will say that it can be pretty frustrating to stumble upon articles written by “too lazy to do any type of real research” authors, who just want to make sweeping generalizations about topics they really know NOTHING about.

I don’t think that helps anybody…

Then again, I don’t know jack shit either, but at least I’m willing to admit that to my readers… I’m still very much learning as I go, so please always keep that in mind.

Rock On!

You have put in a huge amount of effort into this article, I commend you for that. As an Australian I’m very interested in Lithium (along with every other resource Australia has - it helps having a huge landmass with lots of different types of terrain). If it’s as lucrative as iron, coal and oil has been, we’ll do well out of it. Lithium is a funny material, because it combines the positives and negatives of resource companies, but it’s also riding on the coat-tails of technology stocks. 2 different volatile sectors, combining into one raw material. Like you say,… Read more »

http://www.fool.com.au/2016/05/31/galaxy-resources-limited-to-merge-with-general-mining-corp-ltd/

Funny that you brought this up, today this is an article.

FI Fighter,

Your readers may wish to read some of the great work done by Matt Bohlsen on Seeking Alpha on this topic.

http://seekingalpha.com/article/3984654-lithium-boom-analysis-future-demand-vs-supply

http://seekingalpha.com/article/4003048-lithium-miners-news-month-august-2016

Regards,

SD

[…] can find my full thoughts on lithium/clean energy both here, and here, but to quickly […]

You are kidding yourself, lithium batteries requires the metals of Li and Cobalt which are both rare metals. Look, the lithium price as commodity has been more than tripled last five years. The more electrical cars are built, the more they will become more expensive as well as lap tops have been becoming more expensive. Tesla, has not made a dollar profit even being heavily subsidized by governments. Any new products, without the cost being driven down by mass production, will not become main stream consumer goods in a capitalist economy ( less input to produce more output is truly… Read more »