With the economy perceived to be improving, and interest rates still historically low, people everywhere have gotten caught up in real estate fever. I’m no different, and have been doing my best to acquire as many properties as possible! Currently, I’m working on closing my third property within the last year. Clearly, everyone wants a piece of the American Dream, right?

The Message

So, what differentiates me from the masses of other homebuyers? What am I doing that’s so “unique” and “special”? Well, whereas most folks are flocking to secure their own personal residence (the giant house with the white picket fence), my version of the American Dream marches to a different beat — that of freedom.

If you’ve ever read Rich Dad, Poor Dad by Robert Kiyosaki, one of the major points he brings up is that a home is NOT an asset. The book has become mainstream, and I was even forced to read it in High School (kudos to my Economics teacher, Mr. Castro), but apparently the message has still gotten lost in translation.

So, let’s repeat this key point once again:

“A Personal Residence is NOT an Asset!”

The sooner this message gets across, the wealthier you will become!

The Lie

Mainstream media, and even the president are constantly urging American citizens to invest in real estate. They say your biggest asset is your personal residence. This could not be further from the truth. If we go back to the basic definition of what assets and liabilities are, it’s this:

“Assets are things that put money in your pocket.”

“Liabilities are things that take money out of your pocket.”

So, then, how can a personal residence possibly be considered an asset? Owning a personal residence will not make you richer. Every month, you have to pay for: mortgage, property taxes, insurance, repairs/maintenance, etc.

What about the tax breaks for home owners? Yes, it’s true that interest payments are tax deductible. But how could that possibly be considered a wise investment? Would you pay your credit card company interest every month, just so you could reclaim a portion of it come tax season? No, you would never do that. You would use your hard earned capital to invest in real assets like stocks to put money into your pocket, instead.

But hold on. What about appreciation? That’s the ace up the sleeve that all homeowners hold, right? If you’re counting on appreciation to make you rich, you are playing a fool’s game. We only have to look back as far as 2007-2009 to see what can happen to folks who speculate on appreciation to make them rich. If the market corrects and the homeowner/investor can’t afford to make the mortgage payments, the end results won’t be pretty. That’s when the market will get flooded with short-sales and foreclosures. Whether you are a homeowner or investor, playing the appreciation game is akin to playing with fire.

The Numbers Don’t Lie

If you still aren’t convinced, let’s run some numbers to prove why investing in a personal residence is a losing proposition. This is especially true if you live in an expensive part of the country.

Everyday, I see co-workers excited about buying their first home residence. After closing, they truly feel like they’ve made it, and arrived in this world. They’ve FINALLY achieved the American Dream. I don’t say this aloud, but inside I’m thinking to myself, “congratulations! You’ve just signed yourself up to work for the MAN for another 30-40 years.”

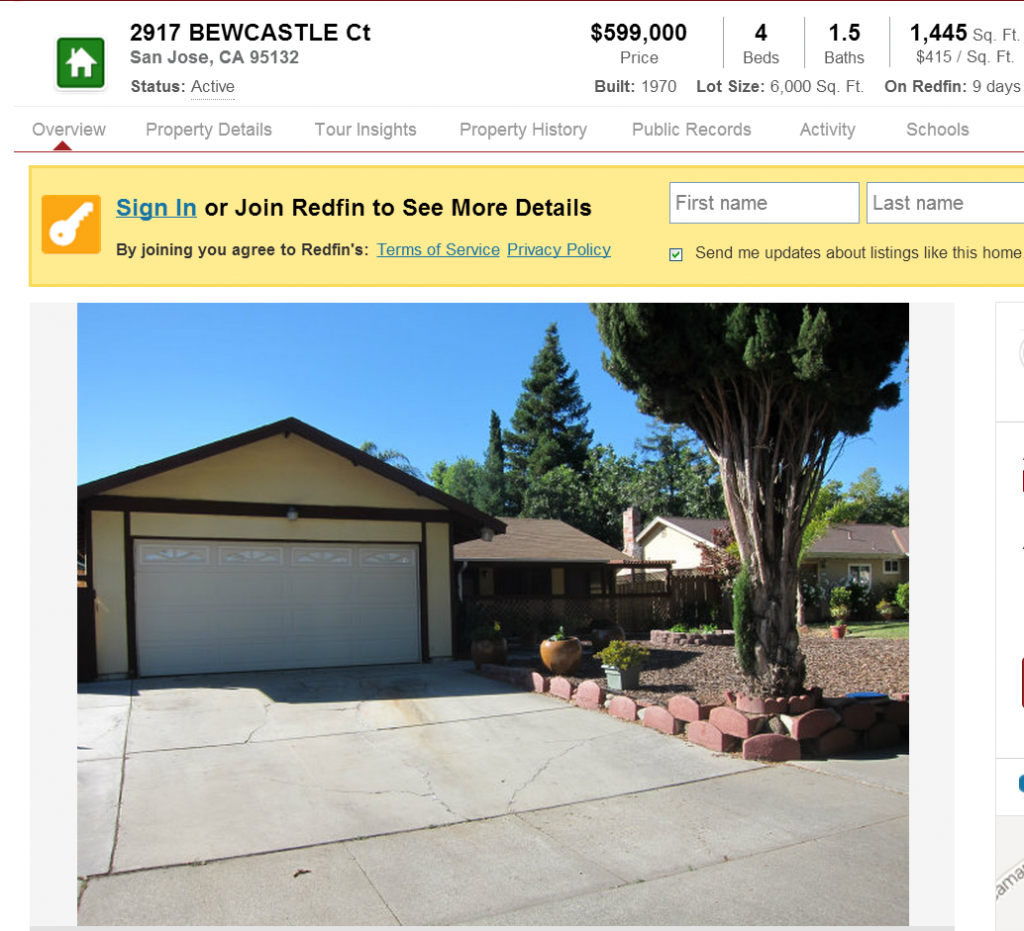

The numbers don’t lie. Here in the Bay Area, a typical single family starter home looks like this:

Again, the price tag might shock you, but this really is the going rate for a starter home in the Bay Area. At $600,000, you really aren’t purchasing too much. It’s a single family home that was built in 1970, in a B neighborhood. The interior is in decent condition, but don’t expect anything remotely resembling turnkey.

So, let’s run the numbers as see for ourselves:

For a 25% downpayment, this requires you to have $149,750 in funds. Further, by “investing” in this home, don’t forget you are now also responsible for $376.25/month in property taxes. And don’t forget the insurance either. When you rent a house, you get accustomed to making a single payment to your landlord that covers everything (plus his profits). 😉 Most new homeowners make the mistake of assuming that the mortgage is their only bill. The total monthly bill ACTUALLY turns out to be $2812.64.

For the above calculations, I’ve left out vacancy and property management since these items won’t apply for a personal residence. For a single family home, you would most likely have to pay for landscaping and utilities, even if you rented, so these numbers really just wash out. They are set to $0 to keep things simple. Maintenance, which used to be handled by the landlord, would be another new expense for the new homeowner. Again, let’s keep things simple and set this to $0.

Rent Instead

Now, suppose you ran the math and realized what a lousy “investment” this personal residence really was. At this point, you’d want to look onto Craigslist or Zillow and determine what the market rates for rent are in your area.

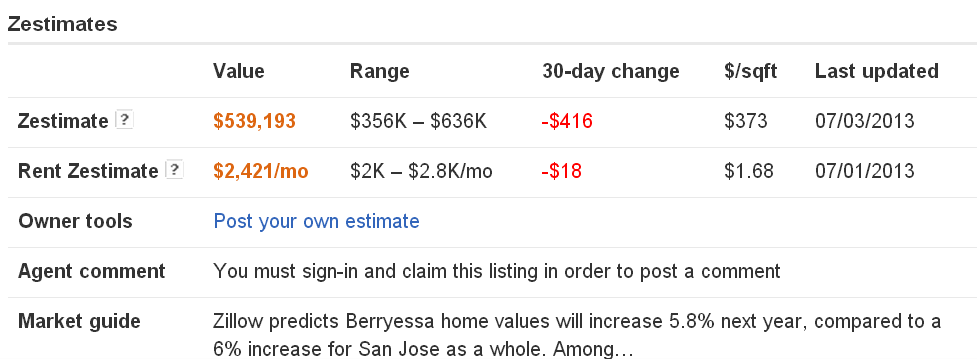

For this property, here is what Zillow found:

Rent is estimated to be $2421/month, which sounds about right for this area in San Jose. So, the difference between renting and buying comes out to be:

Buying: $2812.64

Renting: $2421.00

Difference: -$391.64

In this example, which applies to most of the Bay Area (and many parts of the country), by electing to purchase a primary residence, you will be throwing away about $400/month!

Other Cons

Yes, I realize the interest portion of the mortgage payments can be partially reclaimed during tax time. And I realize you can depreciate the home for 27.5 years, which is why I elected to throw away the maintenance costs. Still, overcoming $400/month difference is no small task.

But that’s not even the worst part about owning. Here are some other cons:

-Fixed mortgage payments. Try missing one mortgage payment, or property tax bill… you’ll see who REALLY owns the house.

-Exit strategy is dependent on state of economy. In a downmarket, you’ll have difficultly selling for “fair” value.

-Opportunity cost. In this example, that’s $400/month in investments you’re missing out on.

-Lack of mobility. You tie yourself down to a particular area.

And the worst part of all…

You’re probably signing yourself up to work another 30 years!!!

The Alternative Play

I often get asked, “How come you don’t own your own personal residence, yet invest in rental property?” The simple answer, going back to our discussion about assets and liabilities, is because my rental properties pay me! When I own a rental, I don’t care about property taxes, or mortgages, or insurance, etc. because my tenants pay for all of that. As an investor, I’m only interested in the bottom line, which is positive cash flow.

So, how would I attack the personal residence conundrum? I wouldn’t. I’d keep on renting. Actually, what I would do is re-define what the “American Dream” really is, and put that downpayment to better use! For myself, the American Dream is freedom. I desire to be free and not have to work for anybody. Owning rental properties will help me achieve this vision, as you’ll soon see.

This is what I would do with that very same $149,750 downpayment:

-Invest in two 2-flats in Chicago ($45,000 each)

-Invest in two single family homes in Indianapolis ($25,500 each)

Total Investment: $141,000

Which would help generate the following revenue:

-Chicago #1: $650.49

-Chicago #2: $650.49

-Indianapolis #1: $443.97

-Indianapolis #2: $443.97

Total Monthly Revenue: $2188.92

Please see this post for more details on investing in out-of-state properties (and for more details on the numbers).

What a HUGE Difference ONE Decision Makes!

Going back to our personal residence example, the Bewcastle property would have cost us $2812.64/month to live in, had we chosen to “invest” in home ownership. By electing to NOT buy, and rent instead, we could pick up that very same property (or one just like it) for $2421/month. By opting not to buy, we instead invested our downpayment into purchasing 4 rental properties. Our rentals now bring in $2188.92/month. Our cost to live in (but not own) Bewcastle has now been reduced to only $211.08/month.

Let that soak in for a minute. Now, instead of making regular monthly payments in the amount of $2812.64 for 30 LONG years, we only need to pay $211.08/month to live in the EXACT SAME HOUSE. Better, we own 4 rental properties that will one day be fully paid off. When that happens, the income stream will become overflowing!

Also, what this does is it frees up our future capital. And that’s really the most important point. Each month, we have an additional $2601.56 (we went from paying $2812.64/month in rent to $211.08/month) we can use to invest in assets, or on anything else we desire!

Rent Free

By accomplishing the above, we’d be able to basically live rent free forever after. We could even eliminate that $211.08 spread by finding another rental that was slightly cheaper. Or, If the local market’s rents increased, we would simply raise rents on our rental properties to offset any differences. It sure is nice to be in a position of power!

So, there you have it. You could follow conventional wisdom, be like everyone else, and be tied down to a mortgage payment for the rest of your life. Or you could continue renting, knowing that this is by far the better financial bet, and invest your capital more wisely elsewhere.

This is exactly what I’m doing. I’m building up my capital each month to buy more rental properties. As the rental paychecks come in, I simply let them snowball and work towards building up for the next downpayment. Lather, rinse and repeat.

In closing, here is a motto I’ve heard and believe to be most true: “Live where you want. Invest where it makes sense.”

The choice is up to you!

That sure does sound great. I’m curious how this would have fared during worse times for rent prices. Say situations when rents are falling. Although I would imagine that can be largely negated by your location choice. I’m not sure I could get the wife on board with this but it’s definitely something to consider. I could probably convince her to let us pick up a rental property or two after we get settled in and as long as they’re cash flow positive then that would effectively lower our mortgage payment on the primary residence. Looks like you’ve got a great plan in place!

I was just thinking about this, but this could be a great way to invest 401k money after rolling it over after leaving work. I know you can invest in property with self-directed IRAs is a rollover IRA essentially the same thing? I’m assuming you can’t take distributions from a rollover IRA so you’d have to convert it to a Roth. I think I might have found a way to tap that money and turn it into cash flow whenever I do leave my job.

Yep, the 401k is a great tool to use. I’ve heard of a lot of people using self-directed IRA’s to purchase real estate.

In my situation, since I already have a few properties, I’d prefer not to use the 401k to buy even more real estate. I think it’s a good idea for someone who wants to get into real estate, but right now, I probably have enough real estate, and not enough stocks.

My 401k admin is also through Vanguard, which has the lowest expense ratio index funds on the market, so I’m not too worried there. I actually like the funds in the plan, and could see myself sticking with Vanguard, even after I leave my employer.

Here’s another strategy I’ve been using — both lender’s I’ve used require 6 months reserve to cover rental property expenses. Usually, after the downpayment, I have very little funds left. I actually use my 401k as “backup” to cover the reserves. So, that’s pretty nifty.

Cheers!

JC,

Just like housing prices, the rent prices would have fluctuated differently from location to location. For my Bay Area, housing prices were slashed by as much as 50%, but the drop in rent hardly moved the needle (maybe just a few hundred dollars, at most). You make a very good point there, and yes, location is of paramount importance. Basically, it’s worth it to pay a little more to get into a market where all the jobs are.

I like Indy b/c it’s a stable market. Sure, you may not get much appreciation, but the prices/rents hold steady, even through the bad times. Bay Area is also very resilient. I haven’t started investing in Texas yet, but the Big 3 (Houston, Austin, DFW) there is also highly regarded b/c that’s where the jobs are! That’s where the people are moving to.

Yeah, the wild card is always going to be finding a way to get the significant other on board… I guess in that sense, I’m lucky being single. I only have me to answer to lol 😉

Cheers!

Being single definitely has its advantages but I wouldn’t change anything. Luckily I live in Texas so it’s easier for me to go and check on the rental properties. I live 30 min from Houston and the other 2 are only 3-4 hours away. Much easier than having to schedule a trip just to check on properties, although I’m sure with the right tax accountant you could count that as a business expense. I started researching a bit on properties in the Houston area just because I think it’d be best if I do get my wife on board I can easily show her the property and she can see it whenever she wants. Texas does have plenty of jobs growth which is why we didn’t suffer too badly during the “Great Recession”. Home prices dropped but nowhere near like they did on the national level.

I’m going to have to research the 401k/rollover IRA a bit more to see what would be best. I’d just hate to have that cash flow locked in a tax advantaged account that I can’t access during early retirement. I don’t think an early withdrawal would be worth it though because I’d lose way too much from penalty and taxes.

JC,

Hey, that’s awesome! You live in perhaps the best area for real estate investing in the entire country. Yeah, I would definitely recommend you stay local for your first investment property. There’s a ton you’ll learn on that first rental, so it’s a good idea to keep it close by. Your wife will probably feel far more comfortable with that as well, as she can keep her eyes on it. I’m sure over time, she’ll be saying, “this is no big deal.”

haha, you’re absolutely right about that tax write off! This is another reason why real estate investing is so great — so many perks. A lot of people strategically invest in areas where they want to go for vacation. So, let’s say you and your entire family take a vacation for 5 days in Disneyworld. If you happen to have a property there, as long as you spend more than 4 hours a day (50% of your time) conducting in some form of business, you can write off: plane tickets, meals, car rentals, etc. These privileges are too awesome to not take advantage of.

There may be ways to get around the 401k penalty/taxes. I’m no expert on this subject by any means, but if you do a search on “401k” on bigger pockets forum, I’m sure you’ll come across a ton of people who have done it.

btw, that forum is gold!

That is exactly what it is a liability. You have to pay for upkeep, utilities, mortgage and everything around. The house won’t bring you any income, unless you sell it later with a huge profit, then maybe you can call it an investment.

People do not have this concept at all. And of course your approach is diametrically different.

Martin,

Exactly, a primary residence won’t be adding money to your pocket, so it doesn’t make you more wealthy.

Of course, home ownership has a lot of other benefits, which might make it still worth owning, but it would be a mistake to call it an asset.

Take care!

A house is somewhere to live, if renting is cheaper, why should you buy? The joys of ownership, it is more like bondage.

Charles,

Yes, it definitely makes more sense to rent if the numbers work out that way. In more expensive areas, this will generally hold true (especially in a rising market).

If more people ran the numbers, they might elect to do something different. It’s the opportunity cost that will get you. That’s a lot of investment money being thrown away…

Cheers!

You may be painting with too broad a brush here. The specific example you include in this entry does not necessarily apply across the board. Real estate is highly variable from one location to another, and from one time period to another. Sometimes by running the numbers the purchase will come out ahead of renting, and sometimes the opposite is true. Also there are benefits to be gained by purchasing that you cannot get from renting (stability, more freedom to renovate and use the land, more predictable monthly payments over time, etc). Plus, once you pay off the mortgage on the primary residence, the monthly cash flow picture looks a LOT different. I can speak to this from experience. So personal residence question (rent vs own) should be considered on a case by case basis.

The ~$2400 rental payment in your example should cover the landlord’s taxes, insurance, mortgage payments, etc (unless the landlord is an idiot). Think of your own rental houses for comparison. Don’t you always charge enough in rent to cover those same expenses, plus leave a little extra for your own profit? So to me, you are paying these expenses on a personal residence regardless of whether you rent or own — the only difference is whether you are paying them directly or indirectly (by way of payments to a landlord).

I think of housing expense similar to how I would think of food expense or any other mandatory expense. In the case of food, you have to eat. You could buy food at restaurants (saving time and labor which can be directed elsewhere). You could buy food at the grocery store and prepare it (less expensive, but more time expensive). You could own land and grow and harvest your own food, then prepare it (possibly even less expensive, but much more labor intensive). Or you could grow food, sell it, and use the sale proceeds to spend on other food at restaurants or at grocery stores (swapping labor for cash). Depending on the specific case, certain people may find any of these options to be the most optimal way to allocate their cash and their time/labor. There is no way to say that any one of these methods is “superior” to the others. I view the personal residence decision with a similar lens.

Having said all of that, it sounds like you have a good system going for yourself. I think the key is that you ran the numbers first, made an informed decision, and understood the consequences (risks/benefits) of your decision. Nice work!

Executioner,

Thanks for the comment. You make some good points, and let me see if I can address some of them.

First off, the article wasn’t meant to bash home ownership. There are a lot of benefits to owning a home, like you mentioned, and I completely understand why someone would want to own their own home. If you want to own b/c you desire stability, ability to renovate, etc., then yes, by all means it makes sense. These things may be more important, and therefore trump the monetary rewards you would get vs. renting. With that said, buying a personal residence should not be seen as an investment. Again, your own home is not an asset.

Yep, I’ll agree with you that my example is an “extreme” case, and that these prices won’t apply across the board. Though I do find the use of an “extreme” example ($600k purchase price) useful in helping me illustrate the main point — opportunity cost. Even if the market rent = monthly payment for purchasing (let’s say it’s break even to rent or buy), I would still call buying a home a bad “investment”.

If you own, you have to make payments every month, let’s say $500, which includes all expenses. I still feel that downpayment money would be better served to buy an investment property that cash flows. Again, the benefits of investing are you have the flexibility to invest in any market that cash flows. You aren’t tied down to just your own backyard. Live where you want, but invest where it makes sense. Let’s say you invest instead, and get $300 in cash flow for that same downpayment. Since rent prices are the same as buying, you rent a home for ($500), and you’re out $200 now, instead of $500. Every month, you would have an extra $300 to invest with. Also, all the interest write-offs, depreciation you would get from your own residence would apply to the rental, so it’s a wash in that regard.

The $2400 example is kind of tricky b/c not all areas cash flow. For my own rentals, yes, the monthly rents are enough to cover all expenses + reserves. Like you said, if it doesn’t the landlord is an idiot 😉 In this example, this property is $600,000 and the rent is only $2400. It not only fails the 1% rule, it fails the 0.5% rule! After taxes, insurance, etc. it would most definitely NOT cash flow. Whoever bought this as a rental is buying a cash flow negative property (unless they put down a huge downpayment, but it doesn’t cash flow at 25% down).

With all that said, one great strategy a lot of people starting out use is this: they buy a duplex or multi-family building. They live in one side and rent the other units. This way, they can minimize or eliminate their own monthly rent payment. Over time, they can sell the unit (to invest elsewhere), or keep it as a rental and move in to their own SFH. The point is, they don’t buy the SFH until their investments are enough to pay for their own rent.

I really don’t think owning a home is “bad.” I just believe most people go about it in the wrong way. Wouldn’t it make a whole lot more sense to invest first, and not own a home until your passive income stream was large enough so that it could pay for ALL your rent and you could live rent free forever after?

Take care!

From following personal finance blogs and forums for the past several years, it seems there are two common ways to achieve FI. One track (the one you’re on) is the highly leveraged approach, rolling income from one asset into the purchase of additional assets (also leveraged). Over time, the cash flow helps to pay down the liabilities. The other track (which is the one I find myself on) is to minimize the liability side of the ledger by eschewing debt and/or paying it down as quickly as possible, then using the positive cash flow to purchase income-producing assets, which evolves into one big debt-free cash-generating snowball. Tales of success from others indicate that both tracks eventually lead to FI with a reasonable degree of success. It is a matter of personal preference as to whether the leveraged approach or the debt-free approach suits your taste.

Based on your careful planning I expect you to be added to the list of success stories in the near future.

Executioner,

You summed that up quite nicely. Yep, seems like there are two distinct tracks one can take to invest towards FI. I started off on the NO DEBT, build up the net worth, buying high yielding (3% to 5%) stocks approach.

Gradually, I’ve switched over to the highly leveraged (10% to 20% cash on cash return) approach.

I don’t think there’s a right or wrong answer. There’s more than one way to skin a cat. Each individual investor just needs to pick the path most suitable for them and their goals. For me, I don’t mind the extra risk, and feel like the potential rewards justify that. I also want to take advantage of more tax breaks which are only possible on the current track I’m on.

Best of luck on your investing journey!

I’ve been watching too many people buy places that cost them more than they were spending in rent. It makes no sense to me. My monthly housing costs are less now than they were when renting by about $200/month and I have an extra 500 sqft. I realize though that it’s not an investment - it’s that I felt buying made more sense than renting for me personally. I refused to buy a place that I couldn’t pay off in under five years, not thirty. I don’t see my place as an asset, but as a prepaid housing thing. So if I end up being a crazy cat lady, I’ll never be making a mortgage payment again soon enough.

I’m curious to see how both of our routes to FI work out since they’re basically the complete opposite, other than high savings rates. Mine is to pay off the mortgage in the next 3 years while maxing out the 401(k) and Roth IRA and stockpile money in taxable index funds after that, which should result in FI in another 5 years after that or so. There are some other reasons that I want to keep working “that long”*, so I’m not that concerned about it.

*One of the many reasons is that I don’t plan to quit my job (at this time) until I have found a long-term partner, regardless of whether I’ve hit FI.

Leigh,

That’s awesome! So, you’re on the opposite end of the spectrum from the example I used.

Home ownership definitely has its perks. I wouldn’t mind owning my own home someday either, I just don’t feel the need for one atm. I think a lot of people just get too emotionally attached with the idea of owning a home that they sort of feel insulted when you tell them, “your home is a liability”. Haha, it’s nothing personal, it’s just the truth! 😉

Yeah, I’m curious myself to see where the paths will lead. I started off working rapidly to build up net worth (like so many others), and have shifted to borrowing money. I’m able to accumulate more valuable assets, but in the process my net worth has gone very negative!

Good luck on paying off the house! That’s quite an ambitious goal, wow, only 3 years, that’s like unheard of.

haha, the more I invest, the more I worry about that long-term life partner thing. At some point, you have to take precautions to protect your assets, right? I guess I still have a few years before I run into that problem. Most girls I’ve dated around 24-28 aren’t into money or saving at all. So, just casual dating for now, since I doubt I could end up with someone who just didn’t care at all about finances. Finding someone else who’s just as gungho about financial freedom… that’s gonna be tough!

Cheers!

Well, four total - I’ve had the place for a year now.

Yeah…I’m definitely worried about the long-term life partner thing. Most of the guys I’ve dated have also been software developers (i.e. high income) and somewhat okay at saving. But the likelihood of me meeting someone who also has a net worth of almost $300,000 at age 25 is not very high… That’s actually part of the reason I want to have my condo paid off so quickly - then it’s very clear in a pre-nup that the condo is 100% mine. At the very least, I’m living in a city that I plan to stay in for a long time. But I pretty much hate dating. Too much small talk, not enough fun.

Leigh,

3, 4… who’s really counting? You’re still moving at the speed of light 😉

The use of a prenup sounds so extreme (like what you’d expect a famous celebrity to do), but probably will be necessary. Yeah, I always figured that I wouldn’t have to do something like that, since I used to envision myself starting wealth accumulation with a partner. This can only get more complicated as the years go by…

I guess I just need to find a “real life” version of you. If I can find someone to get on board this early FI thing, we could tag-team it and be retired YESTERDAY!

Take care!

What, are you saying I’m not real??? 😛 Maybe my city is even somewhere you’d want to move after retirement!

If I met someone with the same net worth as I currently have and the same future earning potential and we spent exactly the same amount as I am now per month, we could retire with the mortgage on my condo paid off by mid to late 2015. That would be SO AWESOME!! So my guess at this point is that I will probably hit FI after marriage if I marry before I haven’t already hit FI.

I dunno, my parents have been harping on me since I graduated from college that I have to get a pre-nup because of inheritance stuff and keeping that separate. I don’t necessarily know for sure I will get one, but I at least want to go through the full documentation process that getting one entails to make sure that both parties know what they’re getting into financially. I’m pretty sure that getting married some day will be the scariest thing I ever do financially.

Your condo wouldn’t happen to be located near the beach, would it? 😉

Let’s see, in mid 2015 I’ll be 30 years old and ripe for retirement! I hope to have 10 rental properties by then, hopefully pulling in $3000 to $4000/month in cash flow. I’m planning on holding onto my Bay Area properties until then, but if they appreciate enough, I may have to trade them in for a few fully paid off properties. That, or upgrade to an apartment building. Some reserves in dividend stocks and cash as well for peace of mind. If I didn’t have to pay for rent (thanks to an awesome like-minded SO), yeah, I suppose I’d be ready to call it a day! $3000-$4000/month should be enough to support two people minus rent.

After retirement, I’d want to travel (for awhile!) to decompress and relax. Eventually, probably get a real estate license and find a way to do that full time.

But I’m burned out now, and just want to get to the fun part! Have you thought about your plans post-FI?

I love this article! It’s not the first time I’ve heard this argument but it never gets dull. I haven’t read RDPD but I happen to live it so I find the statement to be true in my experience. As you know SoCal/OC area has similar price points as the Bay Area. You have to add mello-roos and HOAs on top of that price point as condos & townhomes start at your stated price point above.

We also found 2 additional Fannie Mae/Freddie Mac “insurance” items fees were tacked onto the price tag of some homes - for what I don’t know but it wasn’t PMI. The total additional fees on top of the mortgage payment, home insurance and property tax was $600/month! This assumes your HOA fee doesn’t increase which it does! We’re renting for the price of less than the mortgage payment only for the same unit - savings of over $1,000-$1,500/month. This isn’t even talking about a single family home which easily start at $600k for the same bed/bath you stated above.

I’m very interested in your out of state investing so I’ll need to read up on those posts!