When analyzing a potential real estate investment property, it becomes oh so easy to over-complicate the process. I often feel like the most important thing to do while searching is to find the right property in the right neighborhood. My personal philosophy is that it’s always better to buy the ugliest house in a good neighborhood than to purchase the best looking property in a crummy location.

Don’t Waste Time

With that said, a lot of investors waste a lot of time running the numbers. Some folks will run calculations all day long, until they’re blue in the face, and still not know what to do! We’ve all been bit by analysis paralysis at some point, and most newbie investors make the mistake of focusing too much energy on the math.

Don’t worry about the math. Dedicate your time to finding an awesome property in a desirable location.

Quite frankly, the math behind analyzing a deal is extremely simple. The most important thing to do is not overlook any hidden fees or expenses. So, it’s always important to do your due diligence and err on the side of caution (use conservative numbers). If the property still cash flows reasonably well, you’re good to go!

The 1% Rule

Here’s a rule-of-thumb that is extremely useful (and will save you a lot of time) to use when analyzing a property — the 1% Rule.

The 1% Rule states that the gross monthly income of the property must be at a minimum, 1% of the purchase price.

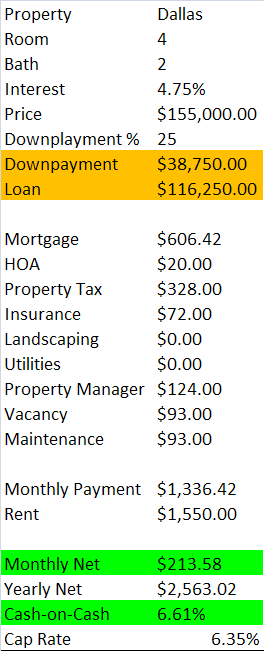

Let’s illustrate with an example property from Dallas.

The gross rent is $1550/month. The purchase price is $155,000. This property exactly meets the 1% Rule.

Dallas is a good example to use because the property taxes and insurance are typically higher than what you’ll find in most other markets. In other words, if the numbers work in Dallas (Texas), they should definitely work in a cheaper location. This example also allocates 6% of gross monthly rent to vacancy and maintenance reserves. Property management fees are 8%. Pretty conservative numbers all around. HOA dues are also included and accounted for.

As you can see, since the property meets the 1% Rule, it cash flows. This isn’t always guaranteed, but I’ve found this to typically hold true. My own personal rule-of-thumb is that if the property fails the 1% Rule, I immediately cross it off my list. There’s no need to waste any more time on such a property, because in today’s market, it’s easy to locate properties that do meet the 1% Rule.

Exceeding the 1% Rule

When I look at the numbers for a property, and I see that the gross monthly rent exceeds the 1% Rule, I immediately get excited. This is usually a good indicator that the property under consideration has a lot of cash flow potential.

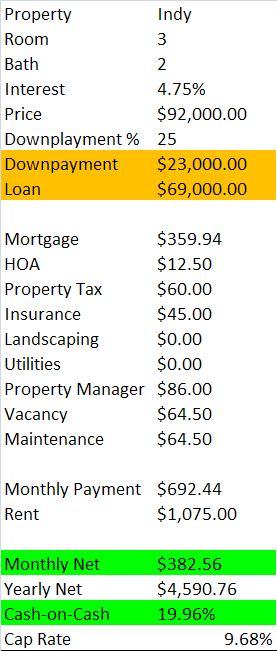

Let’s use an example from Indianapolis.

The gross rent is $1075/month. The purchase price is $92,000. This property exceeds the 1% Rule (1.17%).

Wow, a cash-on-cash return of close to 20%! That’s something to get excited about. Assuming the property is located in a fabulous neighborhood, this is the type of deal I would jump on.

Note: Indianapolis is a market that has lower property taxes and insurance than Texas. Comparing the two directly would be like comparing apples to oranges. There are different reasons (not numbers specific) for investing in each one.

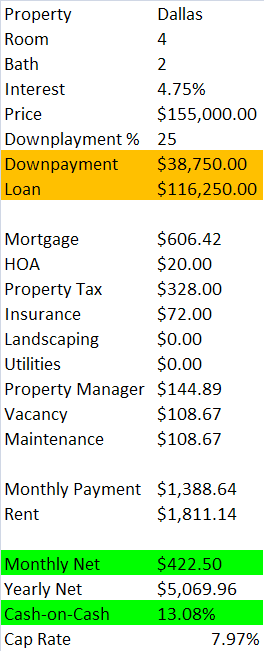

But let’s revisit the same Dallas property and revise the rent to match the 1.17% ratio found In Indy.

Gross monthly rent adjusted to $1811.14. The purchase price remains the same as before, $155,000.

For a market like Dallas, 13.08% cash-on-cash is a very solid return. Again, I would pounce on this deal!

The 2% Rule

Once upon a time (2009-2012), it was possible to locate very desirable single family homes in good neighborhoods that would cash flow so tremendously that they would meet the 2% Rule! That’s right… 2%!!! These days, it’s next to impossible to locate such deals. The rebound in housing prices across the nation have made these deals a thing of the past.

However, if you are daring enough to venture outside of the good neighborhoods, chances are reasonable that you’ll still be able to locate properties that meet the 2% rule. Generally, these properties are priced around $25,000 to $50,000. In many cases, the 2% Rule is achieved because these cheap houses are actually duplexes. If each side rents for $500/month, you can see how it’s possible.

Sub $50,000 properties are what you are most likely looking at though. The odds of finding $100,000 properties that rent for $2000/month are not very good. If you scale up further, the odds of finding $200,000 properties that rent for $4000/month are zero… Yeah, those don’t exist. Rents don’t scale with purchase price as most everyone in the Bay Area, New York, L.A., Seattle, Boston, etc. know.

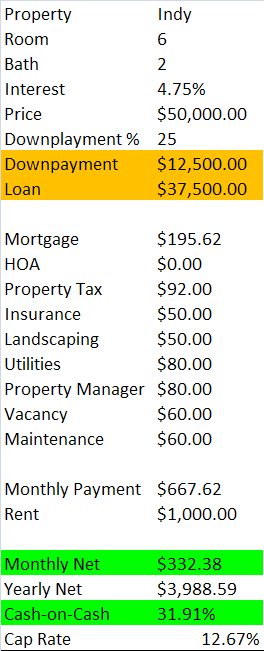

Let’s analyze a 2% Rule deal.

This is a duplex. Each side is a 3/1. The gross rent is $1000/month. The purchase price is $50,000. This property meets the 2% Rule.

With duplexes, the owner typically has to pay for utilities (unless individually metered) and landscaping. However, even with all these extra expenses added in, a property that meets the 2% Rule will still cash flow fantastically. In this example, the cash-on-cash return is an outrageous 31.91%! Honestly, I’ve never ever come across such a deal. The only properties I’ve located that cash flow this well are in areas I would be hesitant to invest in. But maybe you’re a pro and can locate them.. if you do, you’ve just found yourself a cash flowing gem!

Failing the 1% Rule

As I mentioned above, if a property fails to meet the 1% Rule, I won’t even consider it. I don’t like taking risks… Yes, I don’t mind taking on a lot of debt (I want to get to 10 loans), but I consider it low risk if each property meets or exceeds the 1% Rule since they will cash flow reasonably well. In the first example (Dallas), even if you had to reduce the monthly rent by $200/month, you would still break even. And this is with maintenance + vacancy reserves already factored in. See, I told you I’m conservative.

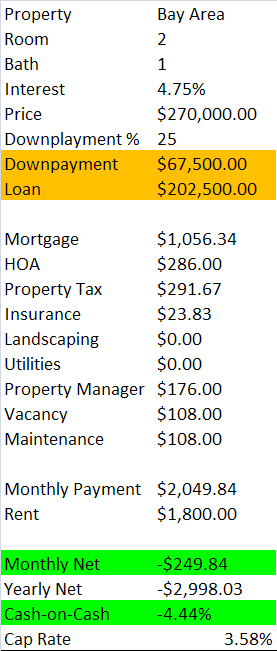

Let’s look at a property in the Bay Area. Well, you can pick any property because they will all fail the 1% Rule these days…

The above property is a real example of the cash flow returns in the Bay Area today. For a conventional downpayment of 25%, the property will not cash flow! Unless you’re buying for appreciation (which should not be considered investing since it’s more like speculation), you really have no business sinking money into this non-investment. You’ll be out-of-pocket $250 each month!

This property fails the 1% rule since the rent to purchase price ratio is only 0.67%. This is a big reason why so many Bay Area investors (and other investors who live in expensive areas) choose to invest their capital elsewhere.

Summary

The math behind real estate investing is very easy and straightforward. You can use the 1% Rule to save yourself a lot of time. This rule will help you quickly filter out properties that are bad investments, since you’ll know right off the bat their cash flow potential without having to dig deeply into any real analysis.

If the property meets or exceeds the 1% Rule, you can then go on to crunch the numbers.

If the property fails the 1% Rule (and you’re not buying for appreciation potential), discard it and move on to the next one.

Math made simple. Happy investing!

You hit on a couple of important subpoints here in addition to the 1% rule, which is, as you’ve laid out spectacularly, very important in my opinion. First, the ugliest house in a great neighborhood. A great location can never be understated with real estate! Location will sell every time, and helps provide for a strong exit strategy. Second, buying for appreciation is speculating. The only exception for this is forced appreciation by rehabbing a property, but that is a whole other ball game when it comes to real estate investing. When looking for buy and hold, it amazes me… Read more »

writing2reality, Yep, I agree. Location is of paramount importance. In fact, many investors (not me) are willing to take negative cash flow and put down huge downpayments for the right area. If you buy in the very best of locations, you’re almost assured strong rental demand. Speaking of appreciation, it’s definitely a game of speculation. As an income investor, I look for strong cash flow. Appreciation is a bonus, but doesn’t factor into my investment decisions right now. However, this may change later in my investing career. For those with deep pockets, it may be worth the risk to buy… Read more »

Fighter, this is a great explanation. I didn’t know it and it sheds a lot of light on the topic. Now I can see why you feel so confident buying more and more property. It’s like dividend investing. You are buying for stable income and do not care what the stock price does meanwhile. I like it!

Martin,

Real estate investing is very much like dividend investing. Dividend investors look at dividend yield and yield on cost. Real estate investors focus on cap rates and cash on cash returns. The main difference, in my experience, is real estate allows you to accentuate (or accelerate) your returns by using other people’s money (OPM). If you look at the numbers above, you’ll see the cash on cash is typically much higher than the cap rate. This is made possible due to the low interest rates of today, which is why I’m such a huge fan of leverage right now.

Happy investing!

FIF,

Excellent post here. I have never looked at real estate in terms of the 1% rule. My condo rental is nowhere near that, however I lived in it first, and paid down a lot of the principal to get is cash flow positive. I also factor in one months rent as a maintenance allowance which cuts my cash flow in about half. But I’d rather be conservative with the maintenance and stash cash.

I am looking to pick up another property and this is very helpful for my analysis. I live in northern Virginia area which is very expensive.

-RBD

RBD,

I agree, it’s a good idea to be conservative with maintenance. I try to run somewhat conservative numbers and still hit 15% cash on cash returns. Obviously, this is a lot more difficult to do in expensive areas, as you’ve seen first hand.

Best of luck on your next property! If the cash flow isn’t there in your local area, perhaps it may be helpful to look elsewhere? I’m slowly branching out, and want to hit Houston and Dallas next.

Happy investing!

How does that 1% rule come in to play if a house your looking at buying needs say $20,000 in repairs to get it rent ready?

Great blog!

Thanks

Peter in Iowa

Peter, There are multiple ways to look at it. I would look at the additional $20,000 in repairs needed as being an addition to the downpayment needed at closing. This would lower the cash-on-cash returns, which I would need to re-analyze to determine whether or not the property was a good investment. As it impacts the 1% rule, if you treat the $20,000 as a one time expense, it won’t make a difference. Again, the cash-on-cash return will be reduced, but the $20k expense won’t increase your mortgage or monthly expenses any. In other words, your monthly net cash flow… Read more »

What sort of financing are you getting or using for these examples?

Aren’t most investors using 30yr @ 8%, 20yr @ 5.5%, I also know some guys using ARM mortgages 5/1 @ 4.765%

Hey buddy, still rooting through all your articles. This is another little gem! I’ve been briefly looking around and am not sure it’s possible to find anything in England that beats the 1% rule that isn’t in a complete hovel of an area. I’m thinking there may be a different rule for UK investors, this could well be for example there is no such thing as HOA here and maybe property taxes aren’t included in rental prices and are paid by tenants. Off to do some googling now! Oh also what is “Downplayment %”? Is that a typo as I… Read more »

Hi FI Fighter,

Very informative article. Thank you for sharing. I am located in the Dallas market and these numbers are certainly accurate. Would you mind sharing your spreadsheet analysis you have illustrated in the article? Thanks in advance,

Darien

The only thing I’m struggling with is that I have a prospective house listed at $33,000. Common rent prices for this house are about $650 a month so nearly 2%. But after calculating taxes, property manager, etc I’ll end up making only about $10 over what I’m putting in. Not worth it?

Thanks for making this so easy. Checking out possible properties for my first investment, and this makes it easy to see if I should even consider the property. One that I’m considering is a triplex and I’m considering moving into it and renting the other 2 out. How does the 1% works with this situation?

Thanks for sharing,

Ryan

Is there a bust in your Cap Rate Calc on your spreadsheets?

I wanted to recreate them and am getting much lower Cap rate when I take Annual NOI/purchase price.

Am I missing something??

Thx!

Keith

Same here Keith. Fi Fighter can you elaborate on the math behind the Cap rates? and also where did you include your closing costs?

Agree, Dan. Having a hard time recreating the math on the spreadsheet. Can you share yours with me?

Thank you Fi Fighter!